Es

EsContainer-lines operating on routes into the U.S. enjoyed a seventh straight month of growth in August, with a 3.6% growth on a year earlier, Panjiva data shows. That was largely the result of increased shipments from Asia, as outlined in Panjiva research of October 9.

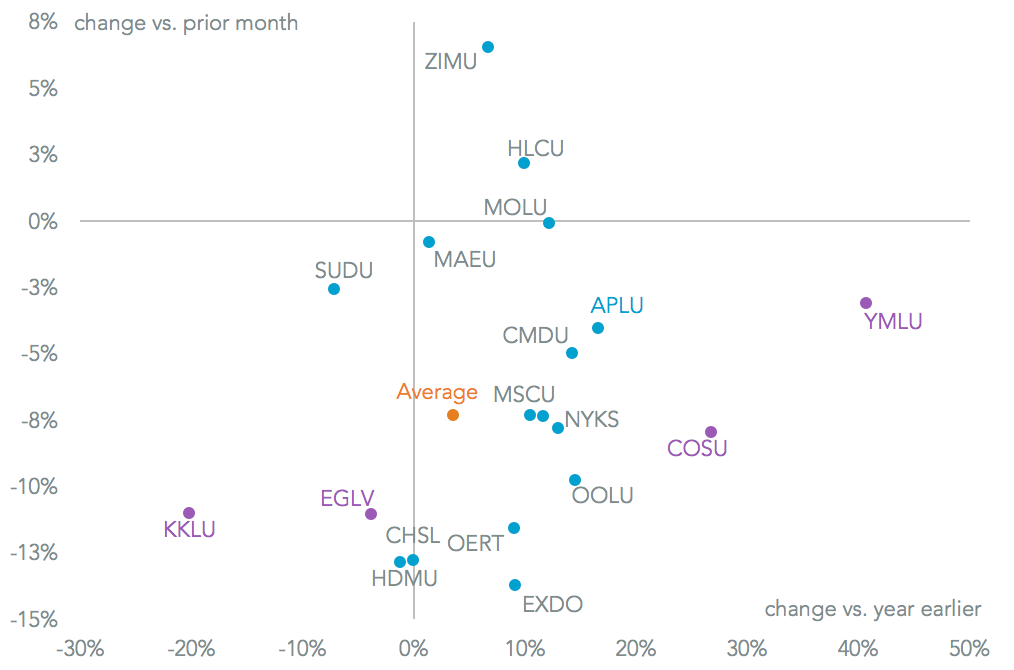

It therefore wasn’t a surprise to see the best performing shippers being Yang Ming (40.7% higher), COSCO Shipping (26.8% better) and CMA-CGM’s Neptune Orient (16.6%). There was still nonetheless clear competition for volumes, as well as restructuring with alliances as Evergreen experienced a 3.8% decline and K-Line a 20.2% slump.

Source: Panjiva

Number one operator MSC continued a surge it started a month earlier with an 11.6% growth in handling. That resulted in a market share for the past quarter of 9.22%, or 0.81% points higher than a year earlier. That should mean it remains the largest operator after the current round of consolidation is completed.

The two current largest deals in progress still have regulatory hurdles to clear. Maersk (which saw a 9 basis point fall in its market share to 6.16%) only has a handful of approvals to go in its acquisition of Hamburg Sud. The combined entity would have suffered a setback after Hamburg Sud experienced a 7.2% drop in volumes, resulting in a combined market share of 7.8% and a net fourth rank.

COSCO Shipping’s purchase of Orient Overseas still faces significant hurdles, potentially including a CFIUS reference due to Orient Overseas’ port ownership. The combined entity would have seen its market share rise to 7.9%, or 1.2% points higher than a year earlier.

Source: Panjiva

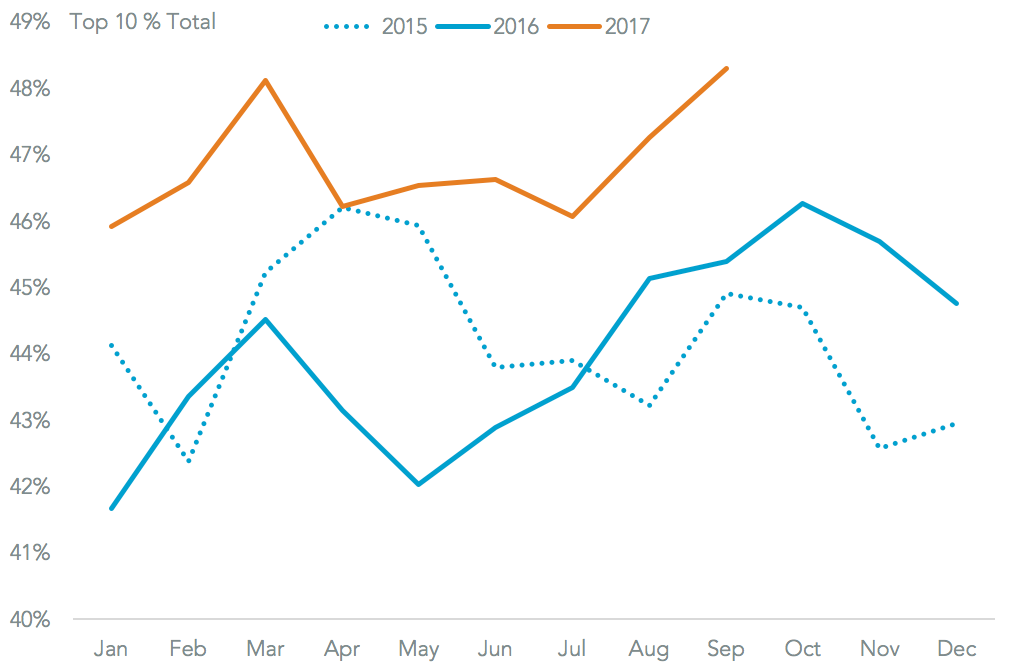

The process of organic consolidation continues too, with the larger operators winning market share from smaller operators. The failure of Hanjin Shipping in August 31 2016 appears to have started a “flight to scale” that’s resulted in the top 10 carriers holding a 48.3% share of shipments in September. That compares to 43.1% for the first quarter of 2016, and was the highest for a single month since at least the start of January 2015.

Source: Panjiva