Es

EsDaily Datum: $74 billion

shipbuilding exports from China, Japan and South Korea in the past 12 months

5 Things You Need To Know About President Trump’s Metal Opportunity

The U.S. Commerce Department has published the results of its section 232 “national security” reviews of steel and aluminum. President Trump has until April 11 (steel) and April 19 (aluminum) to decide whether to apply tariffs or quotas to all imports, or to implement country-specific measures.

(1) The reviews tie into the Trump administration’s national security and economics policies. While employment in the metals industry rose 3% in the past year, it has fallen by 1% annually in the past 20 years.

(2) The steel and aluminum industries accounted for 5% of the U.S. trade deficit, or $41 billion in 2017, so cutting imports could (knock-on effects to other industries aside) meet the administration’s key metric of cutting the trade deficit too.

(3) Taking all the products under review, imports totaled $41 billion in 2017, up 31% on a year earlier. That was well ahead of the 8% annual growth for the past eight years and suggests a “beat the tariff” rush as well as rising commodity prices.

(4) The largest exporters were Canada (26% of the total under consideration in 2017), Russia (7%) and South Korea (6%) while the fastest growing in the past eight years have been Vietnam and the UAE.

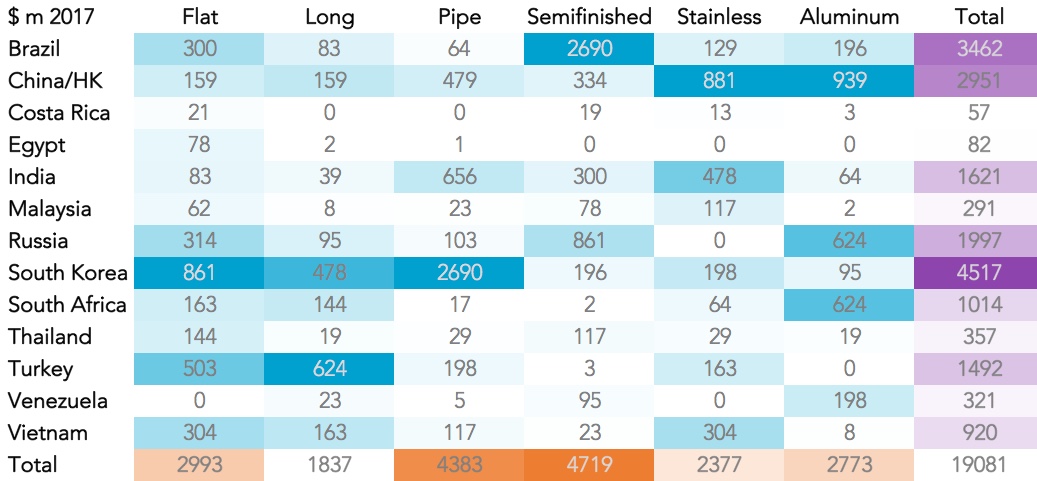

(5) The more targeted measures against 14 countries with higher tariffs may be more defensible at the WTO and could tie into other geopolitical targets. For example the largest exports from China being considered are aluminum ($939 million) and stainless steels ($881 million) while from South Korea they are pipes/tubes and flat steels.

Read more →

Source: Panjiva

UPS Down in Virginia, Exports Have Worst Month Since 2009

Container handling through the Port of Virginia had a poor start to 2017 after volumes fell 4% on a year earlier in January, the first substantive decline in 18 months. The main culprit was a 15% slump in exports – the worst performance since July 2009. Further disruptions are possible as new capacity is installed. Import growth also slowed, and became more reliant on China (6% higher) and the EU (up 5%) after shipments from Singapore and Brazil dropped.

There’s also been a marked rebalancing between the logistics firms servicing the ports. Hapag-Lloyd and CMA-CGM (up 24%) pulled ahead of the 2M Alliance (MSC fell 17%) among container-lines. For the forwarders UPS’s reverse continued with a 29% slide, possibly as it attempts to rebuild profits after a disappointing 4Q. By contrast to the west coast picture Expeditors (19% higher) outperformed CH Robinson (up 1%).

Read more →

Source: Panjiva

Sanyo Joined The Solar Surge Ahead of Japan Filing a Section 201 Appeal

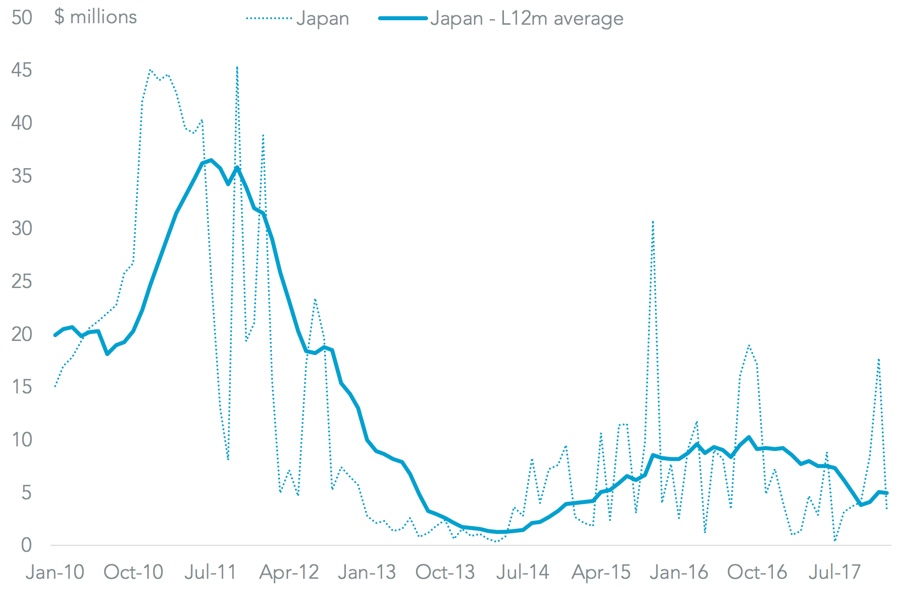

The Japanese government has joined those of China, South Korea and Taiwan in filing a WTO consultation request regarding the U.S. section 201 solar power review. While an expansion of the group isn’t a surprise, Japanese exporters’ share of U.S. imports accounted for just $80 million, or 1.2% of the total in 2017. That may suggest a “point of principle” filing to preempt te future use of the section 201 procedure. While shippers including Sanyo ramped up imports at the end of 2017, they slumped in January and are well below the $434 million peak reached in the 12 months to June 2011.

Read more →

Source: Panjiva

GLOBAL TRADE WRAP

Also in Japan, exports got off to a strong start in 2018 with a 12% increase on a year earlier. That was higher than economists expected and was due to a 23% surge in machinery exports and a 31% rise in shipments to China. The latter looks set to continue given the results of recent manager sentiment surveys. The problem remains the U.S. While exports only rose 1% in January, the 12 month trailing trade surplus was 5% higher than a year earlier at 6.97 trillion yen ($65 billion). That will cast a continuing pall over trade discussions led by Vice President Pence. (Panjiva Research – Industries)

The shipbuilding industry’s rollercoaster continued in January with a 7% drop in exports from yards in China, Japan and South Korea. That was the result of a 22% slump in shipments from China, which is hardly a surprise given the trough in orders reached last July. COSCO Shipping may be called upon to further expand its fleet to support Chinese yards, as Hyundai MM has done for South Korea. Total exports in the past 12 months – a proxy for total fleet growth across all shipping sectors – climbed 10% to $74 billion. (PanjivaResearch – Logistics)

Coming back to steel, the U.S. ITC has confirmed that exports of steel wire rod from Ukraine and South Africa were dumped in the U.S., and so duties should be applied. The case – which also covers other countries – has only been partly successful. Although shipments from Ukraine and SA ended in August, total imports only fell 15% in the fourth quarter on a year earlier. The future for such cases will be complicated by the outcomes of the section 232 review referred to above. (Panjiva Research – Industries)

The U.S. Commerce Department has also been petitioned to investigate alleged circumvention of tariffs – via partial transformation – against Chinese exports of hardwood plywood. Circumvention may be the least of the American producers’ problems after seaborne imports surged 70% higher in January vs. September to reach a new record. An acceleration in shipments from south America may be a response to improved market pricing after the exit of Chinese manufacturers. (Panjiva Research – Industries)

After a lackluster 2017, including the failure of Toys’R’Us and U.S. import growth of just 2% – the toy industry is focussing on how to improve efficiency in its supply chain. While there is the potential to adopt methods used in the “fast fashion” sector, there’s no getting away from (a) the low value-to-volume ratio that makes seaborne shipping the most economic delivery method and (b) the importance of the holiday selling season. Shipping schedules became more condensed in 2017, with 15.8% of annual imports in October vs. 15.3% in the prior seven years. Spinmaster and WowWee have both experienced delivery challenges in the past two years. (Panjiva Research – Industries)

Trade price inflation in the U.S. accelerated again in January with import prices rising 4% and exports by 3%. While that is predominantly due to higher prices, it still suggests a further rise in the trade deficit. When the import price rise is put together with an 8% increase in seaborne imports there is the strongest signal of a surge in imports since April 2017. (Panjiva Research – Industries)

NAFTA Watch: The next round of negotiations, due to start February 25, will start with the hard work of dealing with automotive rules of origin and agricultural market access. As discussed in our 2/09 analysis these – along with standards such as state procurement and “sunset” provisions – appear to be the main sticking points for a successful conclusion to talks. (Bloomberg)

The South Korean government is continuing to become more hawkish regarding trade relations with the U.S. President Moon Jae-in has reportedly referred to the process of renegotiating KORUS as being unfair as U.S. law has primacy over the agreement, which in turn has primacy over South Korean law. That comes on top of the solar panel complaint made by the Korean government at the WTO (referred to above) and another regarding steel and power equipment outlined in our 2/14 research. It all bodes ill for the next round of KORUS negotiations. (Yonhap)

Staying with troubled trade deals, the CPTPP trade deal is far from complete despite the signing of a final text, as analyzed in our 1/24 report, with national ratification yet to be completed. Canadian Trade Minister Francois-Phillipe Champagne has indicated that Parliamentary bill won’t be ready until “after the summer”. That’s unlikely to change the deal, or give the U.S. time to re-enter it, but does illustrate how prolonged final implementation is likely to be. (Bureau of National Affairs)

Container shipping prices for routes out of China improved for an eighth straight week with a 1% rise vs. a week earlier ahead of the lunar new year break. Pacific basin routes were strongest with a 1% rise in rates to the U.S. west coast and 3% to South Korea and southeast Asia. With trade activity remaining robust, as outlined in our 2/15 report, there’s no reason for improvements not to continue though the timing of the holiday will distort pricing for the next few weeks. (Shanghai Shipping Exchange)

Maersk has alluded to the potential for involvement in further consolidation in the container-line sector at its capital markets day, with plans for “inorganic” growth and a statement that “consolidation is important, it’s part of our strategy”. Consolidation remains a necessary process for the industry to rebuild long-term profitability, as discussed in our 2018 Outlook, though regulatory intervention will become more likely as the operators become bigger. (Maersk)