Es

EsThe start of the 3Q corporate earnings reporting season has brought another crop of comments and concerns from company management teams about the impact of volatile trade policy issues including the tariffs in the U.S.-China trade war and Brexit.

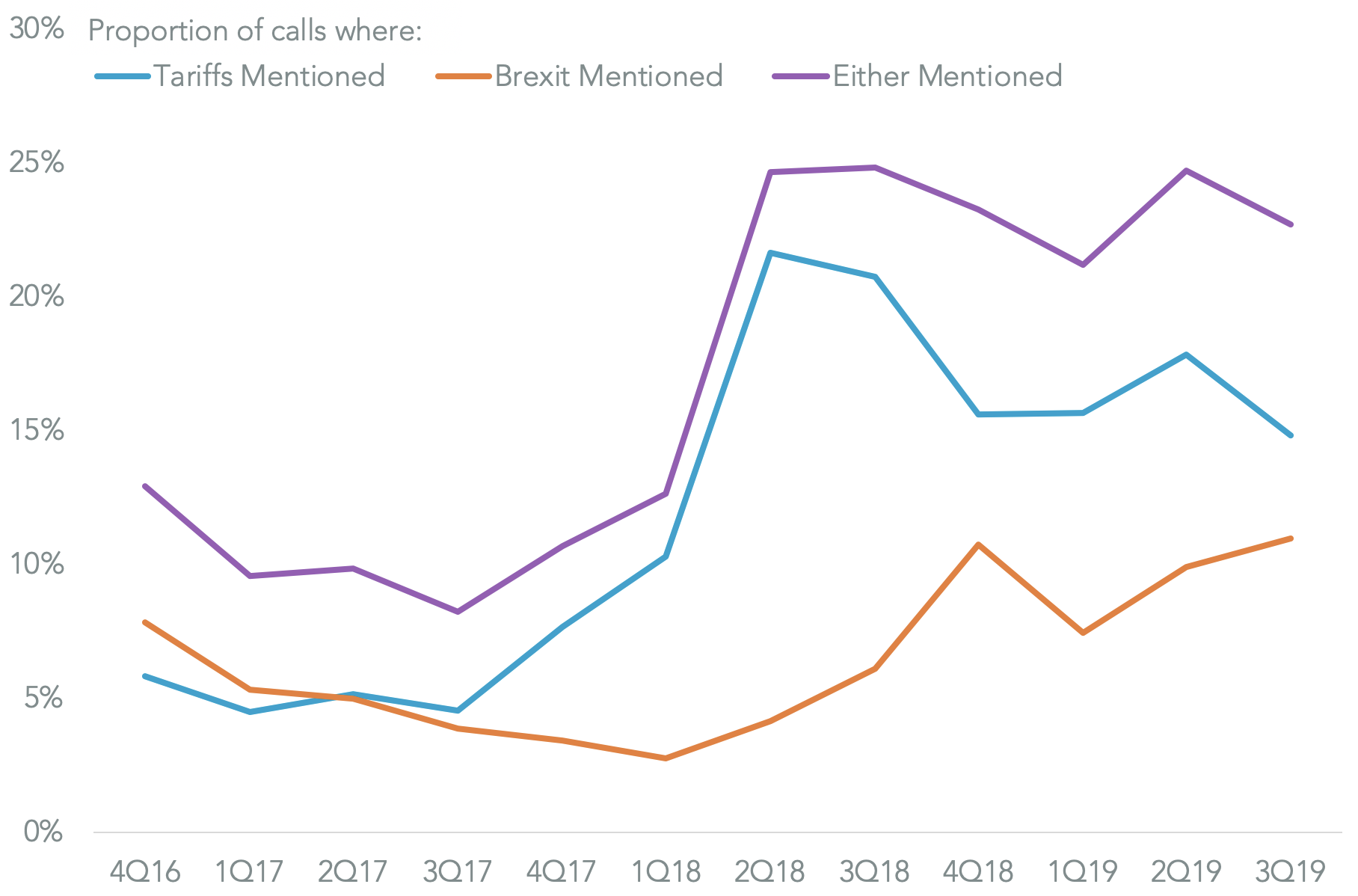

Panjiva’s analysis of 1,142 calls transcribed by S&P Global Market Intelligence since Oct. 1, 2019 shows 22.7% mention either tariffs or Brexit, down from 24.7% in 2Q calls. While that would suggest a reduced interest in trade policy, it’s worth noting that the same group only represents around 1/7th of calls that will likely occur, and is biased towards the financials and non-hardware technology sectors which have had little to say historically anyway.

The downturn may also reflect a vacuum of firm news for company management teams to discussed. As outlined in Panjiva’s research of Oct. 21 remains in limbo, though the rate of mentions has increased to 10.9% of calls from 9.9% in the prior quarter – the proximity of the theoretical Oct. 31 exit date has likely helped.

Similarly the outcome of the U.S.-China “phase one” trade deal remains intangible, making forward-looking commentary more challenging than usual.

Source: Panjiva

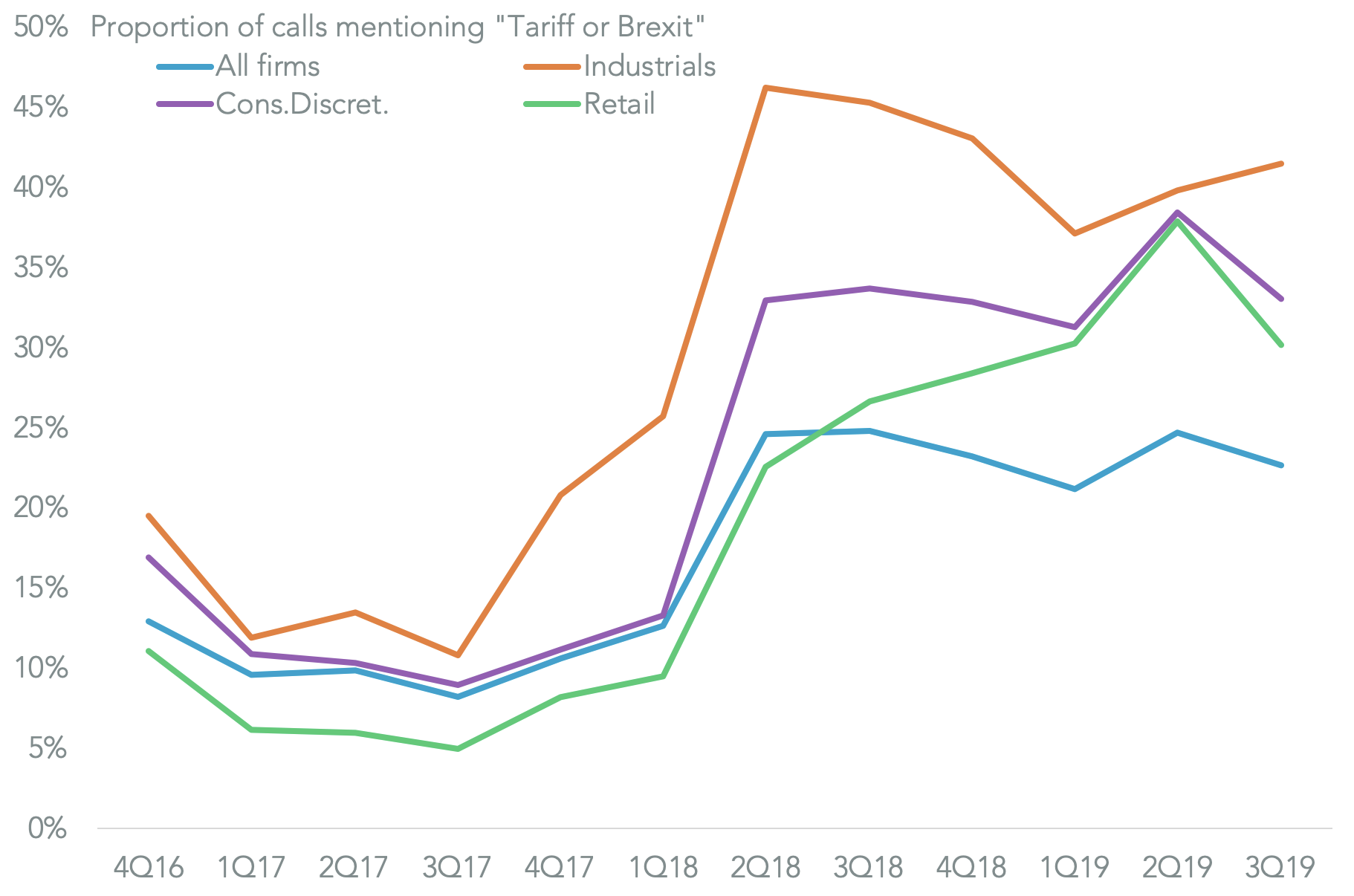

Among the major sectors, the Industrial remain most preoccupied with trade policy, with 41.5% of calls so far this quarter mentioning either tariffs or Brexit. That was followed by consumer discretionary with 33.1% with retail (both discretionary and staples) at 30.2%.

The expansion of tariffs into the consumer space in early September, and the prospect of a widening to all products by mid-December may lead to an increase in discussions of tariffs in the consumer-related industries during the quarter.

Source: Panjiva

Concerns in consumer space apply to appliance makers including iRobot, which saw its stock price fall as much as 19.0% after the company altered its tariff strategy, Bloomberg reports.

The firm had previously increased prices to pass on tariffs. However it’s competitors didn’t follow suit so in order “to drive consumer demand and defend our category leadership, we rolled back prices to pre-tariff levels earlier this month”, CEO Colin Angle stated. So far “it appears that this tactic has helped improve sell-through levels” according to Angle, perhaps providing a template for other firms that have pursued price rises.

Panjiva data shows that iRobot has nonetheless seen its U.S. seaborne imports outpace peers in 3Q with a 10.6% year over year rise versus 4.2% for all seaborne imports of vacuum cleaners. Yet, iRobot’s imports dropped 2.4% in September alone, which may feed into weaker 4Q sales whereas its peers grew by 8.0%.

Both Bissell and Sharkninja did better in September with 12.2% and 17.3% increases in shipments respectively,. The main loser has been Miele which saw a 27.6% slide in imports associated with the firm. That may reflect a higher cost base despite the imposition of tariffs on its competitors given 89.3% of its imports in 3Q came from Germany, similar to a year ago, with just 9.6% coming from Hong Kong.

Source: Panjiva