Es

EsPanjiva’s research motto is that supply chains never sleep – that’s certainly been the case for the policy underpinnings for global supply chains over the 2019 holiday period. This report – one of four looking at policy, logistics and industrial supply chains – looks at the major policy developments outside the U.S. in late December, the data-driven conclusions and the implications for 2020.

The Brexit process continues apace after the British Parliament passed the Withdrawal Agreement Bill with a comfortable majority. That will lead to the start of a transition period from Feb. 1 through Dec. 31. As outlined in Panjiva’s research of Dec. 20 that will include negotiations on future trade relations including both customs and trade agreements in the context of wider economic and security relations.

Yet, there are early signs of a potential delay to the process. European Commission President Ursula von der Leyden has flagged the potential need for talks beyond Dec. 31 as “time is extremely short for the mass of issues that have to be negotiated“, Reuters reports. From a technical perspective the European Commission may not have a Parliamentary mandate to negotiate until March.

Talks may start on a hostile footing. While Prime Minister Boris Johnson has stated that the U.K. will not request an extension, EU Trade Commissioner Philip Hogan has said he doesn’t “doesn’t believe prime minister Johnson will die in the ditch over the timeline for the future relationship“, according to The Irish Times.

There may be an increasingly pressing need for the U.K. to ensure continued export growth to the EU though. Panjiva’s analysis of official data shows exports to the EU from the U.K. fell by 2.8% year over year in the three months to Oct. 30 despite two months of improvements. That’s led to a 0.1% decline in the past 12 months after three years of expansion in sterling terms. The EU meanwhile has seen continued growth in its exports to the U.K. and so may be in less of a rush to act.

Source: Panjiva

A new year also brings new tariff schedules. China’s Finance Ministry has cut rates on 859 products under WTO most-favored nation status rules, Xinhua reports. That continues an annual process of tariff rate reductions that is likely designed in part to help economic stimulus. In context the 850 reductions compares to 706 tariff lines cut in Jan. 2019 and 8,549 HS-8 tariff lines in aggregate.

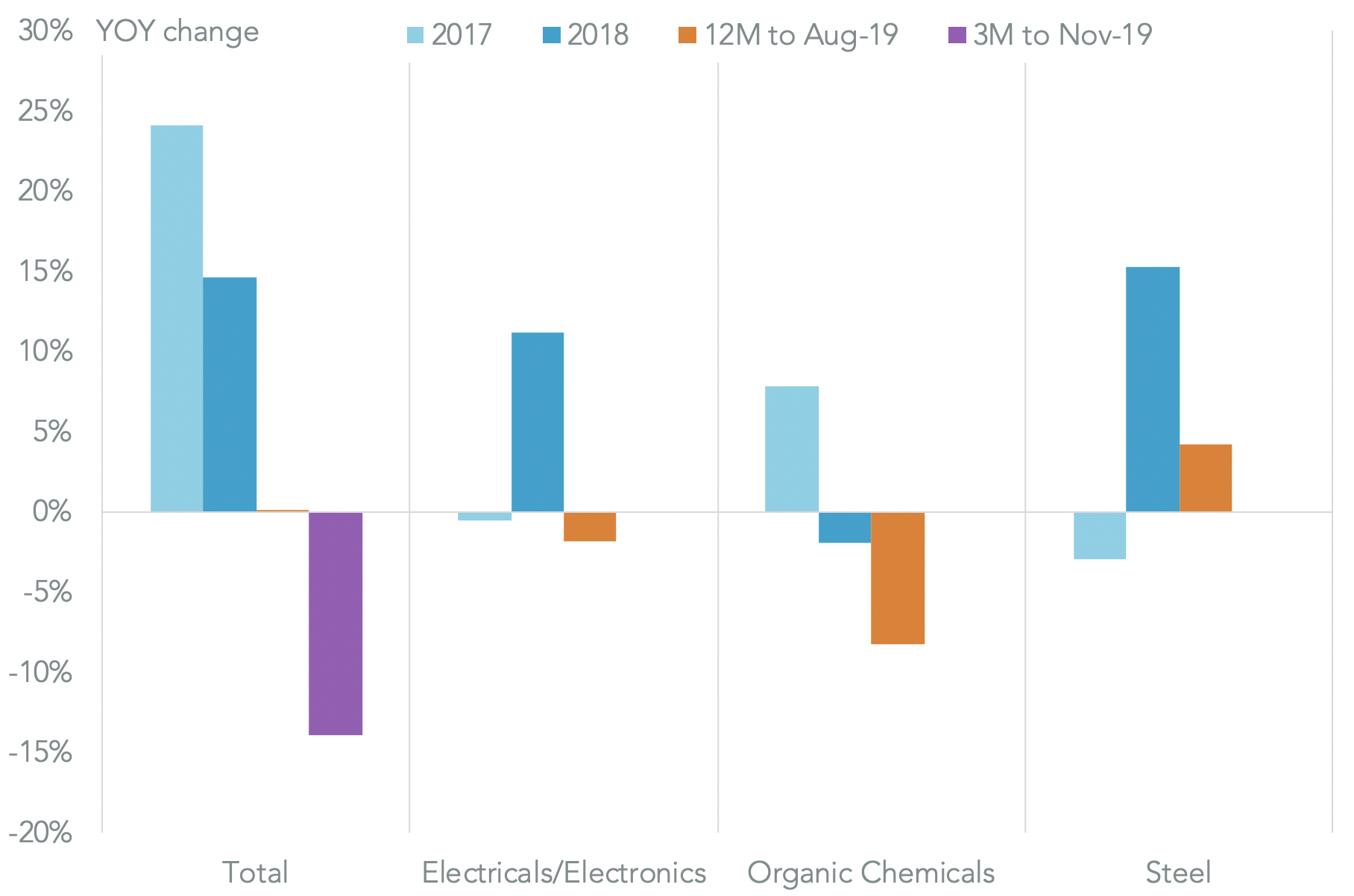

India by contrast may be set to increase its import tariffs once, according to Economic Times, more with four government ministries – including those covering chemicals, heavy industry, IT and steel – looking for ways to cut imports via higher tariffs.

Existing tariff policies under the “Make in India” program have already been partly successful though. Panjiva’s data shows Indian imports of organic chemicals fell by 8.2% year over year in the 12 months to Aug. 31, while shipments of electrical and electronic products declined by 1.8%. One area for action may be steel, where shipments have increased by 4.3% over the same period.

Total imports meanwhile have continued to decline, with a 14.0% year over year drop in the three months to Nov. 30, Panjiva’s analysis of official data shows, though that’s been down to commodities in large part. Wider tariffs make rejoining the RCEP trade deal even less likely

Source: Panjiva

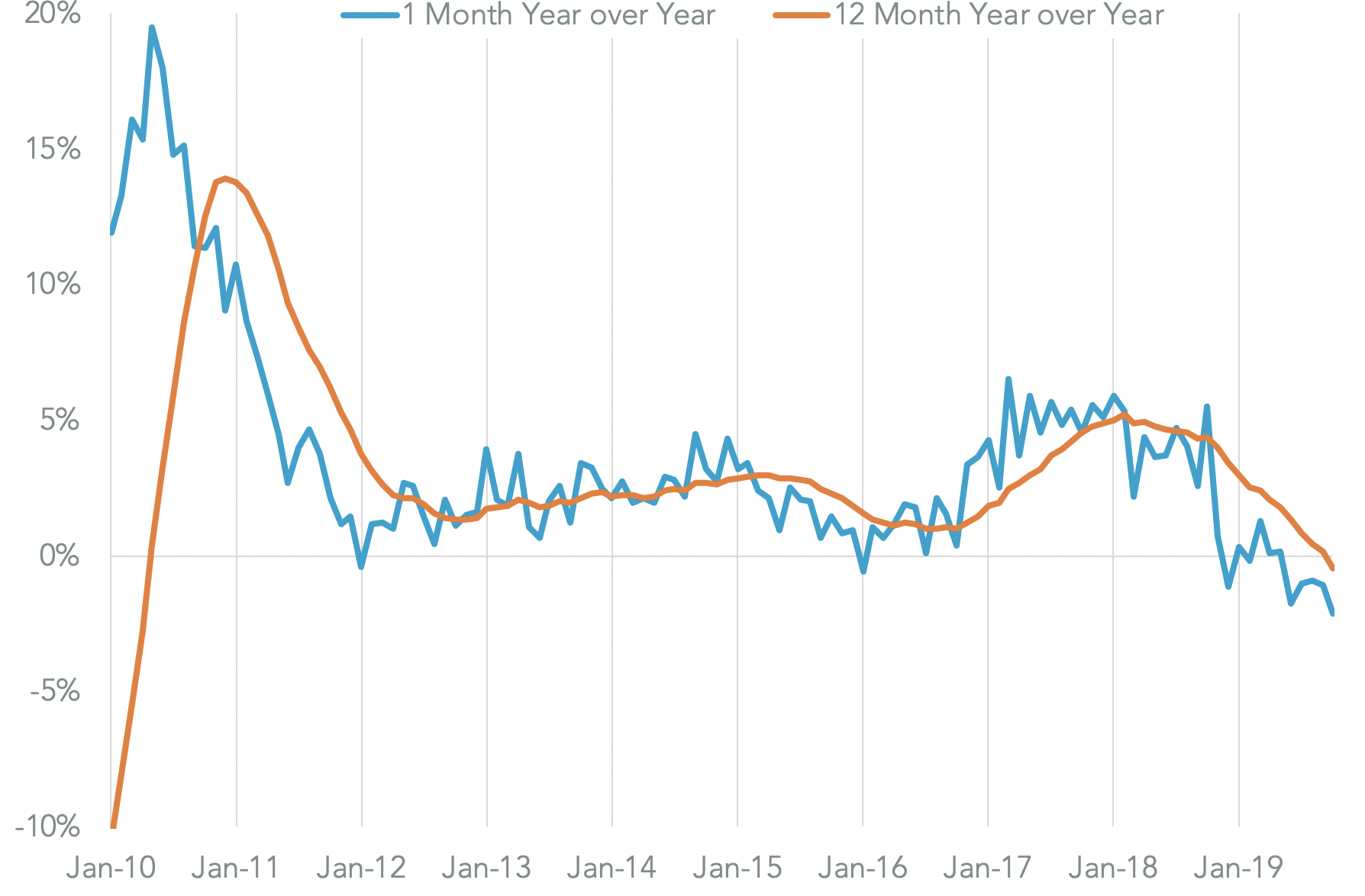

Tariff-driven attempts to boost trade come after a parlous year for international trade activity. Global trade activity fell by 2.1% year over year in October, Panjiva’s analysis of CPB World Monitor data shows. That marked the fourth straight month of decline and meant the 12 month average of a 0.5% decline was the first annualized drop on that basis since April 2010.

There probably wasn’t an improvement at the end of 2019. Panjiva’s analysis of S&P Global Market Intelligence data shows 17 out of 24 countries that have reported November data saw a decline at an average rate of 2.9% year over year.

Source: Panjiva

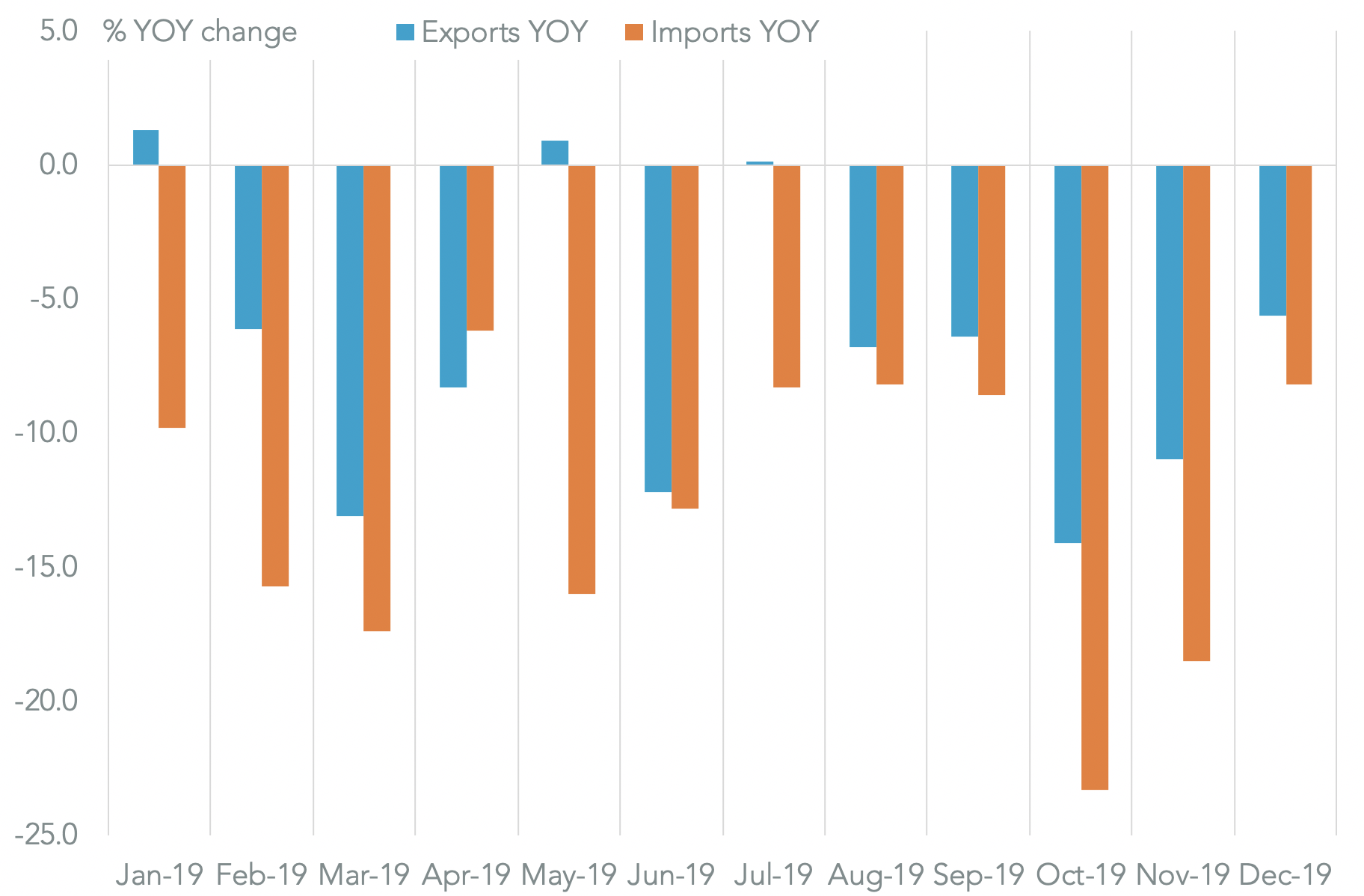

Similarly, exports from South Korea, typically the first country to report monthly data, fell by 5.2% year over year in December, Panjiva’s analysis of official data shows. That was the slowest rate of decline since April and the slowest since December 2018 when excluding the volatile shipping industry with a 1.4% decline. Yet, it still marks the 13th straight month of falling exports.

While the bulk of South Korea’s trade downturn has been due to sliding semiconductor exports, which dropped by 17.8% year over year in December and by 31.5% in the prior three months, regional political tensions with Japan have not helped. Japan has continued to “lose” in that regard, with South Korean exports to Japan down by 5.6% (compared to 9.3% in the prior three months) while Japanese exports to South Korea fell by 8.2% (versus 13.9%).

There have been moves towards resolving those tensions, Reuters reports, though there have been no major policy moves following a meeting between President Moon and Prime Minister Abe on Dec. 24.

There may be some hopes of a rapprochement on a wider basis though after a tripartite meeting between Japan, South Korea and China to try and restart a normalization of relations between North Korea and the U.S. according to Nikkei. In terms of regional tensions, at least the threatened “Christmas surprise” from Chairman Kim Jung-un of North Korea has been avoided despite a worsening of rhetoric towards the U.S.

Source: Panjiva