Es

EsEstée Lauder reported calendar Q2 (fiscal Q4) revenues which dropped by 32.0% year over year as a result of widespread store closures linked to COVID-19. The beauty products manufacturer noted that at the end of June around 15% of retail stores in Europe and 20% in the Americas remain closed.

The firm expects calendar Q3 (fiscal Q1) revenues to decline by 12% to 13% year over year. That partly reflects the continued impact of COVID-19 as “some retail locations in certain markets may not reopen” as well as “restructurings and bankruptcies in the retail industry“. The latter has already been prevalent in the apparel and multi-line retailers as outlined in Panjiva’s research of Aug. 17.

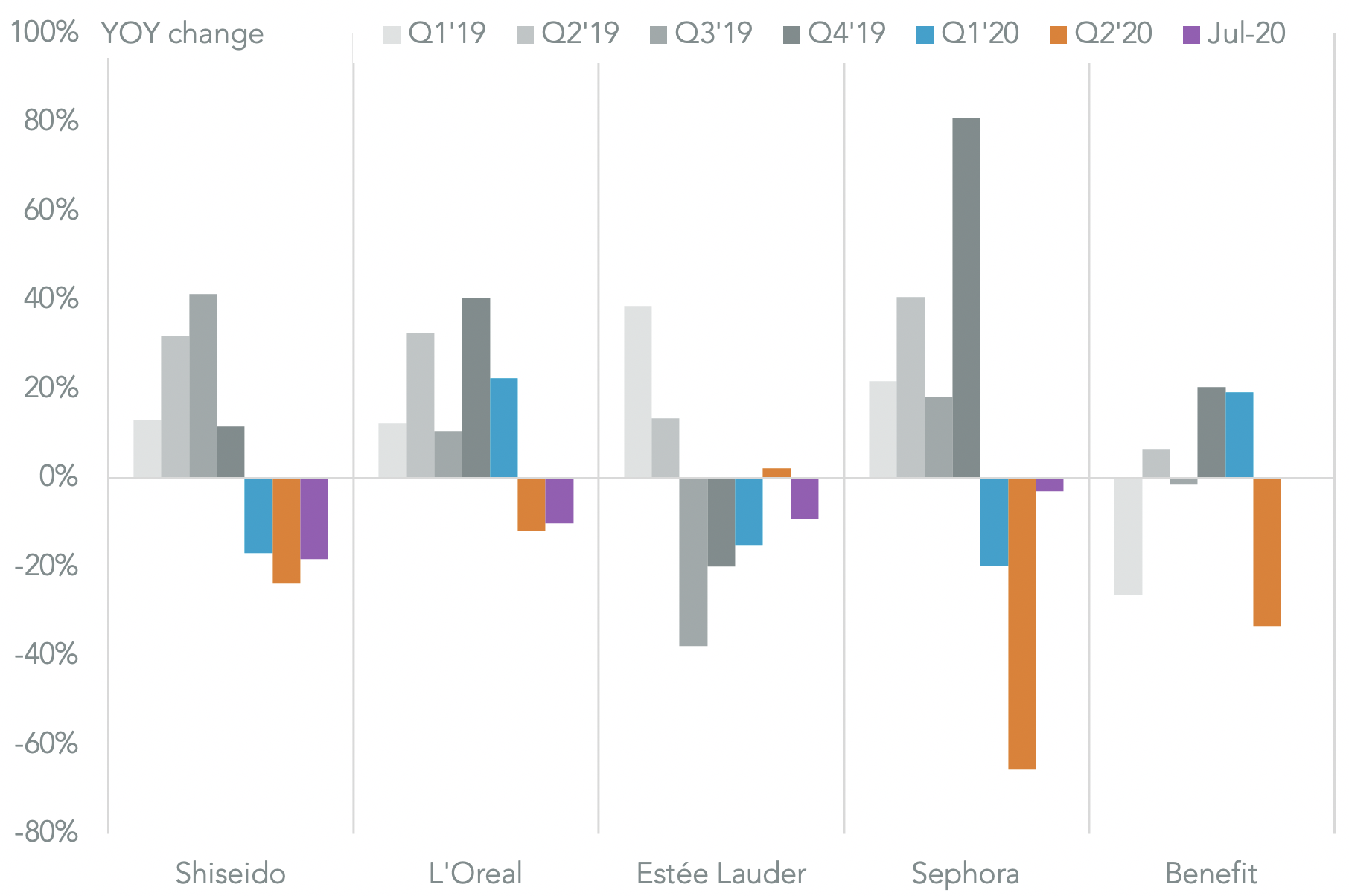

Given the later-than-average reopening of stores in the Americas it is worth examining progress in Estée Lauder’s U.S.-bound trade. Panjiva’s data shows that U.S. seaborne imports linked to Estée Lauder support the potential downturn indicated with total shipments linked to the firm having fallen by 9.6% year over year in July.

There was a 2.2% increase in shipments in Q2 which may reflect a degree of stock buildup. Indeed, the firm’s inventory days rose to 246 days from 210 days a year earlier, S&P Global Market Intelligence data shows.

Source: Panjiva

Most of Estée Lauder’s have seen a similar downturn in July with shipments linked to L’Oreal down by 10.2% while Shiseido’s fell by 18.2%. Smaller brands have done somewhat better though with shipments linked to Sephora down by just 2.9% while Benefit’s were unchanged. Yet, both Sephora and Benefit’s shipments had fallen significantly in Q2, by one third and nearly two thirds respectively, suggesting inventories were already under control.

Source: Panjiva