Es

EsK+N has joined 6 of the 8 forwarders in reporting profitability that was worse than expected in 4Q. Hapag-Lloyd meanwhile has hit is highest margins since before 2013 and is best-in-sector. The EU rattles its (steel?) saber, but will need the WTO to beat back Trump’s tariffs. Also: Japanese automotive exports improve; weakening Chinese business sentiment; BPA plastics tariffs; catfish at the WTO; section 232 decisions are close; President Trump’s Annual Trade Agenda; Californian dairy subsidies; and a potential India-U.S. trade deal.Daily Datum:

Daily Datum: 40%

NYK’s share of Toyota’s Japan-to-U.S. car shipping

NEED TO KNOW

K+N Joins Peers With Great Revenues, Disappointing Profitability

Freight forwarder K+N reported 4Q revenues that climbed 19% on a year earlier, and were 5% better than expected. That repeats the pattern seen from all the other freight forwarders that have reported so far. In common with Expeditors that has been driven by a surge in airfreight. A 15% rise in seafreight handling may not be repeated after U.S.-inbound volumes fell 3% in January, while the company has guided to a 4% to 5% growth for the year.

Yet, the growth in revenues came at the cost of falling profitability, which fell to a 6.1% EBITDA margin from 6.6% a year earlier. All but two of the eight forwarders to report so far (Fedex and XPO) saw a similar pattern of falling margins, suggesting pricing discipline is still needed across the sector.

Read more →

Source: Panjiva

Hapag-Lloyd Hits a High, Has Room To Be More Aggressive

Container-line Hapag-Lloyd reported an 11% rise in 4Q revenues vs. a year earlier. That was 1% below analysts’ expectations, whereas the other liners who have reported so far have all done better. That was the result of underlying volumes (excluding the effect of UASC being consolidated) being unchanged vs. a year earlier. A slower rate of growth may have continued, with U.S. inbound volumes up by just 3% in January.

However, the lower revenues were likely due to disciplined pricing. When combined with cost cutting that resulted in a profitability (EBITDA margin) that reached the highest since at least 2013 of 13.7% vs. 10.1% a year ago. It’s also the highest in the sector having pulled ahead of Maersk and Matson. If anything the rising profitability suggests Hapag-Lloyd management may have room to become more aggressive in chasing market share in the rest of 2018.

Read more →

Source: Panjiva

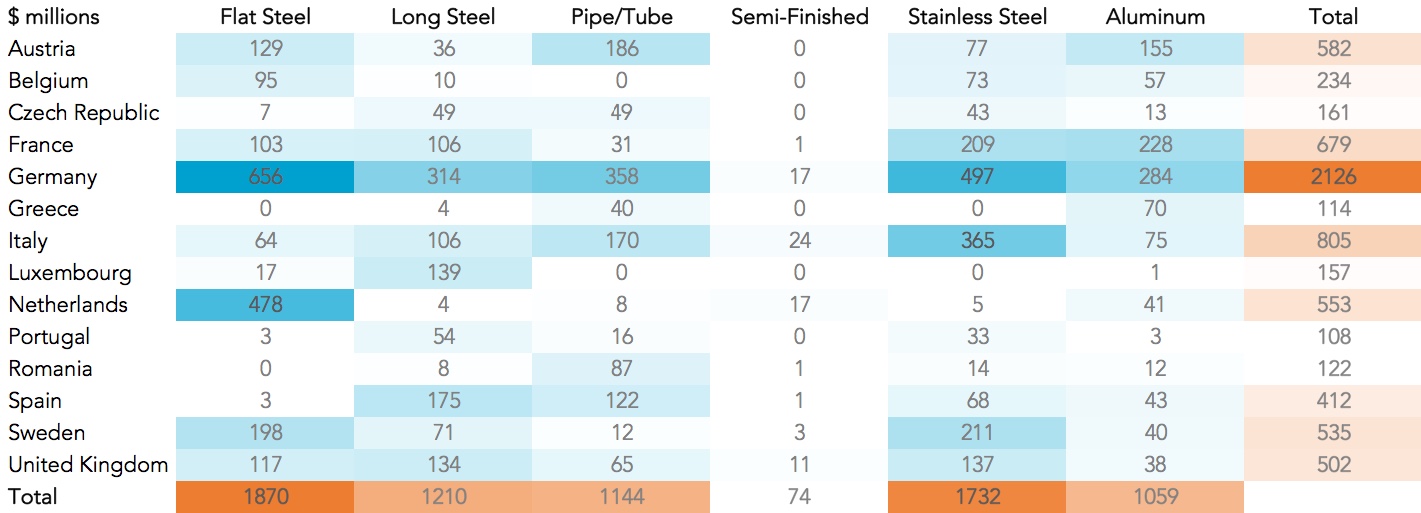

Malmstrom’s Metal “Countermeasures” May Need WTO Support To Be Effective

The EU is “ready to take countermeasures” against U.S. steel or aluminum tariffs due under the section 232 review. That’s not a big surprise, and repeats comments made by Trade Commissioner Cecilia Malmstrom in June 2017. The EU is significant supplier of the products under review, accounting for $7.3 billion of shipments to the U.S. in 2017, or 16% of the total.

While the European Commission has primacy in deciding trade policy, it’s worth noting that Germany is the most exposed country. It exports to the U.S. totaled $2.1 billion, led by flat steel and stainless steel products. The room for retaliation in steel and aluminum is limited though. The EU only accounted for 6% of U.S. exports, or $2.8 billion in 2017 even including the U.K. That would suggest a WTO-reference with tariffs across other products would be the most fruitful route for action.

Read more →

Source: Panjiva

GLOBAL TRADE WRAP

Japanese automotive export growth is accelerating, with a 6% expansion in January from the big seven automakers. Mazda led the way with a 34% surge following the start of production of the MX-5, while number one producer Toyota rose 13%. Improved sales in the U.S. may be helping, with seaborne shipments up 6% in January. The growth should be a boon for the car carriers, though competition remains fierce. NYK is Toyota’s number one carrier with a 40% share in the past year, but saw a 7% drop in volumes in the fourth quarter as Mitsui OSK caught up. (Panjiva Research – Industries)

The Year of the Dog may be off to a rough start after Chinese business sentiment on exports fell into negative territory for a second month. That would suggest a slowdown lies ahead after 11% growth in exports in January. Of more concern for trade across Asia is that import expectations also turned negative to reach their worst since August 2016. (Panjiva Research – Industries)

While much of the focus in trade policy currently is on the big-ticket items (more on that below) and trade deals, regular trade cases continue and can have a significant impact on supply chains. The Chinese Ministry of Commerce has applied duties of up to 31% on Thai exports of plastics precursor BPA. That came after imports only fell 3% in the fourth quarter vs. the first, suggesting the initial threat of tariffs was insufficient to deter shipments. Furthermore the tariffs were backdated after a spike in shipments in November. Makrolon and the local subsidiaries of Mitsui and Mitsubishi will have to pay more for their plastics. (Panjiva Research – Industries)

It’s not just industrial cases that need to be watched. Vietnam has launched a WTO complaint after being “unfairly targeted” for duties on catfish exports to the U.S. Vietnam accounted for 95% of U.S. exports last year, with a 41% drop in shipments in the past three months on a year earlier. At the same time the cost of catfish, shown by average import values per ton, has risen 30% in the fourth quarter. (Panjiva Research – Industries)

President Trump may unveil his decisions on tariffs / quotas under the section 232 review of steel and aluminum today. That follows the posting of recommendations by the Commerce Department that include both blanket and targeted approaches, as well Presidential commentary about the industry having been “decimated”. As discussed in our 2/19 research targeted tariffs may be more defensible at the WTO, but the latter may preempt circumvention or country-hopping. At the same time Vietnam has joined the EU and others (see more above) in threatening retaliation against the President’s actions. (Washington Post, White House, Vietnam News)

The President also launched an updated Annual Trade Agenda. Compared to last year it leads off on national security as the top priority, which wasn’t a specific feature last year as outlined in our report of 3/01/2017. That ties into both the section 232 reviews (which are “national security” investigations) and potential section 301 action against China. Last year’s top priority, “sovereignty over trade policy” shifts to the bottom of the list, and instead refers to supporting reformation of the World Trade Organization. (U.S. Trade Representative)

NAFTA Watch: Yet another front in the agricultural battles between Canada and the U.S. has been opened. Canada has launched a WTO dispute regarding Californian support for the dairy industry. That comes as agricultural arguments form the centerpiece for the current round of NAFTA negotiations, shown in our 2/22 analysis. (Inside Trade)

One target for U.S. trade policy has been to launch bilateral trade negotiations with other countries. That looks set to start with an agreement with India to launch free trade talks at a forthcoming “2+2 Ministerial” meeting scheduled for April 18. The process includes engagement by the State and Defense Departments rather than Commerce and USTR though. India has several trade policy irons in the fire currently, but – as analyzed in our 1/25 research – is also implementing a swathe of new tariffs to support domestic manufacturing. (Bloomberg – paywall)