Es

EsWe investigate Maersk’s acquisition options in container-lining. With the section 232 review of steel and aluminum having been published, we look at the retaliation risks. Container handling through Savannah is slowing – we discover why. Also: Expeditors had a strong 4Q; Exxon’s expanding its PNG LNG; the EC is reviewing U.S. bioethanol; Ontario calls for “fairness in procurement”; the Commerce Department’s 2022 strategy allows for more 232 reviews; EU and Mexico are struggling to complete their trade deal; but South Korea and CAFTA have managed to secure their deal.

Daily Datum: 29%

rise in ONE’s shipments to Savannah in January, had it been in operation

NEED TO KNOW

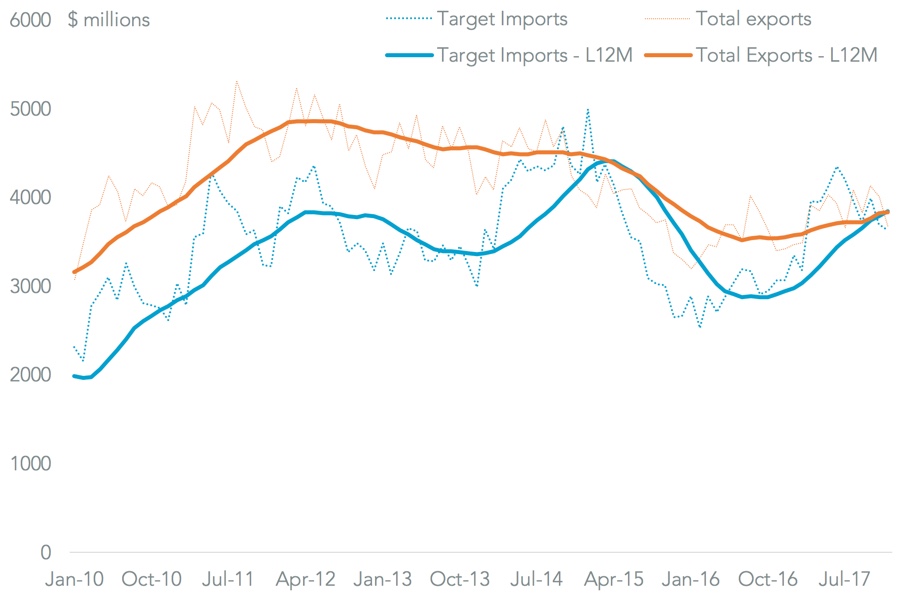

Maersk Could Look East For Its Next Deal, But Faces Pricey Options

Container-line Maersk has stated an intent to make further acquisitions, stating “consolidating is important, it’s part of our strategy”. The acquisition of Hamburg Sud was a good fit in terms of routes, opportunity for rationalization as well as being financially.

With regards to routing Maersk’s next move could be towards Asia. In terms of U.S.-inbound shipping it is under-represented in Taiwan (0.9% of volumes vs. 3.5% for all liners) and Japan (0.9% vs. 2.3%). That would suggest Evergreen, Yang Ming or Ocean Network Express would be a good fit.

ONE is too big – it has an enterprise value of $30.1 billion vs. Maersk’s $51.6 billion and the $4 billion purchase price for Hamburg Sud. Evergreen and Yang Ming are nearer the size of Hamburg Sud, but are currently trading at 11x and 20x EV/EBITDA vs. the 8x paid by Maersk for Hamburg Sud. Another option is to acquire elsewhere in the logistics sector, though several freight forwarders are already committed acquirers too.

Read more →

Source: Panjiv

American Bolts and Plates Could Pay The Price For Chinese s232 Retaliation

The U.S. section 232 review of steel and aluminum imports is already drawing threats of retaliation, even before President Trump has decided on what actions to take. China has made it clear it will “take necessary measures to protect its own rights”. Those could range from WTO consultations to direct retaliatory tariffs.

While the Commerce Department has already acknowledged the risk of such – hence the country-specific options as well as broader tariffs – there’s no reason why retaliation would be limited to equivalent products. Exports of all steel and aluminum products to all countries were worth $46 billion in 2017. That’s the same amount as the imports of specific products being protected by the s232 case, and would suggest a targeted approach would make more sense.

China imported $2.7 billion of steel and aluminum products from the U.S. in 2017, up 17% on a year earlier. Outside of aluminum scrap (39% of the total, which will likely drop anyway due to waste import restrictions) the main products that could face retaliatory tariffs include steel bolts/fasteners and aluminum alloy plate.

Read more →

Source: Panjiva

GLOBAL TRADE WRAP

Container handling by the Georgia Ports Authority rose for a 15th straight month, but the 2% rate was the slowest since that run of growth began. That was due to an 8% slump in exports, which was also seen in Virginia and California. Imports remained strong though, with a 10% rise driven by shipments from China. Ocean Network Express (ONE) would have been the biggest shipper into the port on a post-merger basis, and also increased volumes by 29% in aggregate vs. a year earlier to overtake both CMA-CGM and Hapag-Lloyd. (Panjiva Research – Logistics)

Staying with activity in the logistics industry, Expeditors International reported 4Q revenues that rose 16% on a year earlier. That was 6% points better than analysts had expected – repeating a pattern seen across the freight forwarder sector – due to strong airfreight volumes. An unwillingness to engage in aggressive competition in ocean freight was seen in a rise of just 1% in volumes, but also in profitability that was 0.5% points better than forecasts at the EBITDA margin line. That was a marked contrast to other forwarders including UPS and CH Robinson that delivered disappointing results. (Panjiva Research – Logistics)

ExxonMobil and Total will double the output of their liquefied natural gas (LNG) operations in Papua New Guinea. China is likely to be a major target market, as it has been for U.S. exporters including Cheniere, with the main potential customers being CNOOC and Petrochina. Yet, PNG exports to China were just 6% of the total in 2017 as the lion’s share of Chinese demand growth went to Australian (42%) and Qatari (23%) suppliers. (Panjiva Research – Industries)

Also in energy, the European Commission will review duties on U.S. exports of bioethanol to determine whether they still pose a threat to EU producers. The duties have been effective so far, with American producers accounting for under 1% of EU imports. Yet, total exports from the U.S. expanded to a four year high in December, with exports dedicated to supplying Mexico and Canada (56% of the total). (Panjiva Research – Industries)

NAFTA Watch: The regional government of Ontario has introduced a “Fairness in Procurement Act” that would allow it to implement barriers against U.S. companies from states that restrict the ability of companies from Ontario to bid for government contracts. This has an equivalent in, but will also greatly complicate, Canada’s national negotiating stance for NAFTA. As outlined in our 2/14 report, major sticking points ahead of the 2/25 round of talks include state procurement, along with dispute settlement and rules-of-origin. (Government of Ontario)

The U.S. Commerce Department’s 2018-2022 strategy includes the provision for implementing further section 232 “national security” reviews to follow the metals and aluminum cases referred to above. There’s already a petition for a review of uranium imports, discussed in our 1/17 analysis, that has yet to be acted upon. Notably though the need for additional resources to support more “self-initiated” regular trade reviews (antidumping and countervailing subsidies) is not referred to. (Commerce Department)

Discussions between the EU and Mexico to finalize their free trade deal have continued to make progress, with the most recent round having closed five chapters. Yet, as is the case with NAFTA and as flagged in our 2018 Outlook for global trade deals, the talks continue to be bedevilled by a lack of agreement on agriculture and rules-of-origin. (Reuters)

Another trade deal that has made progress is that between South Korea and CAFTA (five central American countries including Panama) which has now been signed. It is a traditional tariff-cutting agreement. The deal is notable as renewal negotiations South Korea’s trade deal with the U.S. are underway, while our 2/01 analysis shows CAFTA’s is unlikely to receive calls for review on the U.S. side. The agreement between the two may complicate talks with the U.S. (MOTIE)