Es

EsThe U.S. Congressional Subcommittee on Coast Guard and Maritime Transportation has raised concerns about consolidation among the container-liners as well as the FMC’s regulation of them. Chairman Duncan Hunter (R) stated on April 4 that “Recent action by the FMC has U.S. industry concerned the limited exemption (from antitrust rules for shipping alliances) is being misused”. Congressman DeFazio (D) called for the legislation allowing the exemption to be reviewed.

In written testimony from FMC Acting Chairman Michael Khouri there did not appear to be an appetite for ex-post reviews. Rather that it would “monitor the marketplace more carefully than ever” now the new alliances have started and “strengthened” the economic review of new alliances. Khouri noted in questioning that the alliances are designed to be operational rather than price-setting in nature, and that the HHI (measure of concentration) of Trans-Pacific rates is lower than the global average.

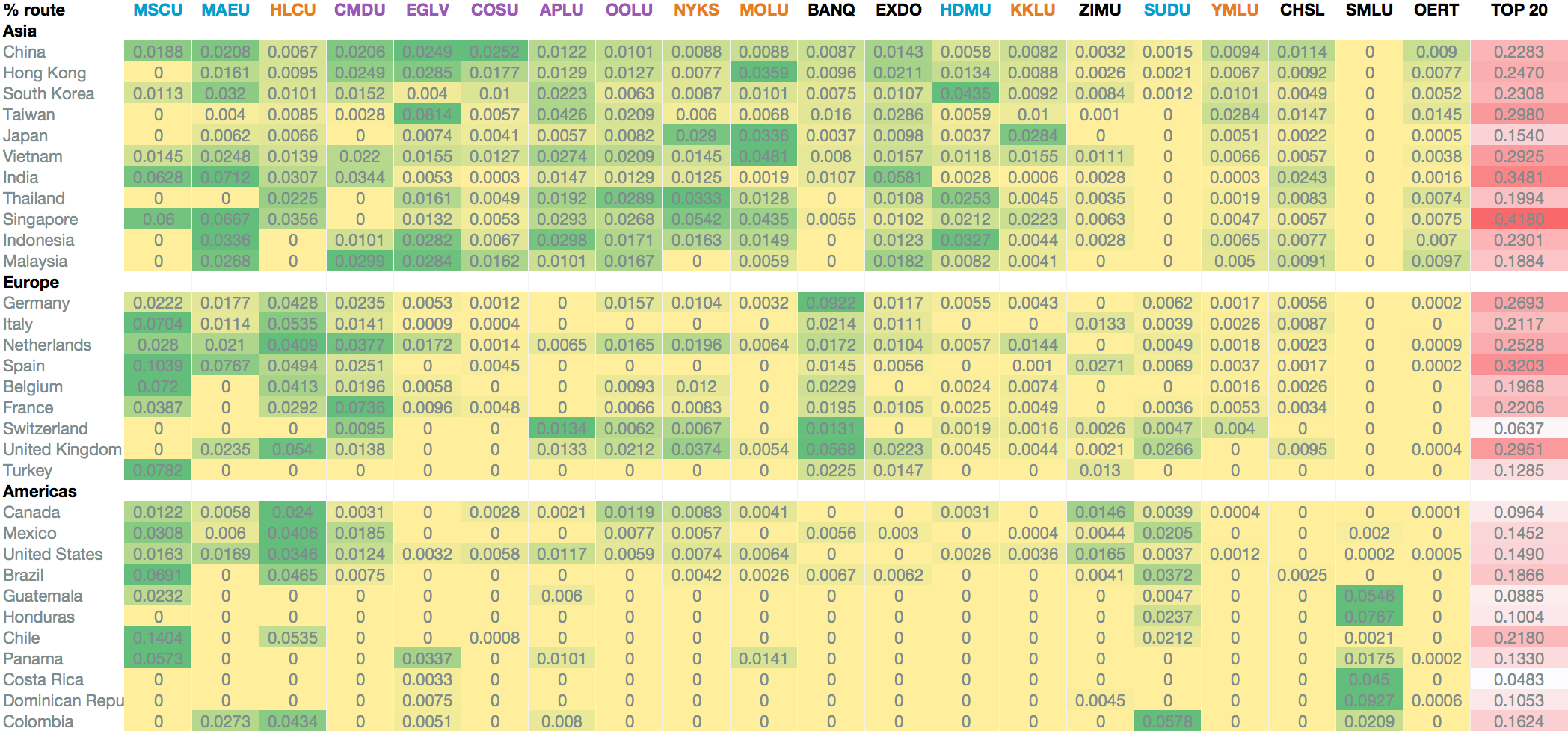

Looking on a more granular basis, Panjiva analysis of the top 20 shippers’ routes shows two factors. Firstly, the level of competition varies drastically by route. On China-to-U.S. routes the top 20 only account for 22.8% of traffic, but for Singapore it is 41.8% and Spain 32.0%. Second, the scale of the operators are uneven – the top five players are twice the size of the next five and four times the size of the following 10. That is exacerbated by only six of the top 20 operators not being in an alliance

The challenge comes at the same time as the Department of Justice has subpoenaed the container-liners, though it isn’t yet clear what case they may bring, as discussed in Panjiva research of March 22. There are also complications for the 2M Alliance from Maersk’s purchase of Hamburg Sud (especially after the recent route deal with Hyundai MM) and for THE Alliance with the merger of the three Japanese liners “3J”.

Source: Panjiva