Es

EsDSV Panalpina reported Q1’21 revenues which jumped 23.1% year over year while EBIT climbed 195% higher. That’s a similar expansion rate to that seen by K+N, as discussed in Panjiva’s April 27 research, and DP-DHL and has been driven by the Air & Sea division’s 45.5% increase in constant currency terms.

Notably though the volumes handled by the firm in ocean freight lagged the market with growth of just 1% versus a market expansion of 5% to 7%. That indicates a reliance on the recent surge in shipping rates to deliver earnings growth.

The increase has been the result of continued congestion in global shipping networks that have affected all major freight forwarders. Notably, Flexport’s VP of Ocean Freight, Nerijus Poskus, has stated “it’s not getting better, it’s getting worse” in reference to Transpacific trade according to Freightwaves, and that loadings are so difficult that “price doesn’t always even matter anymore“.

Panjiva’s data shows that U.S. seaborne imports linked to DSV Panalpina climbed 42.4% higher year over year in Q1’21. That was only partly linked to a post-pandemic recovery, with the expansion also being equivalent to a 27.1% rise compared to the same period of 2019.

Operations on Transpacific routes, where much of the expansion has been focused, saw volume growth of 110.2% year over year in Q1’21, equivalent to a 62.1% increase versus Q1’19. The latter was faster than the 75.9% expansion experienced by Flexport on Transpacific routes, though the latter continued to grow at double- or triple-digit rates throughout 2020 with volumes ending up in Q1’21 being 444.4% higher than those in Q1’19.

Source: Panjiva

The continued expansion in Asian trade activity has led DSV Panalpina to announce the acquisition of Global Integrated Logistics from Agility for $4.2 billion. The deal adds 23% to DSV’s revenues in a full year and extends its footprint across emerging markets in the Asia Pacific and Middle East regions.

Consolidation in the freight forwarding industry had slowed somewhat during the pandemic and subsequent volume boom before SF’s purchase of a stake in Kerry in February.

DSV had nonetheless remained committed to further expansion in the fragmented freight forwarding sector as recently as the firm’s Feb. 21 earnings call. With other forwarders, particularly those with stock market quotations, less focused on scale there may not be a challenge to DSV’s bid.

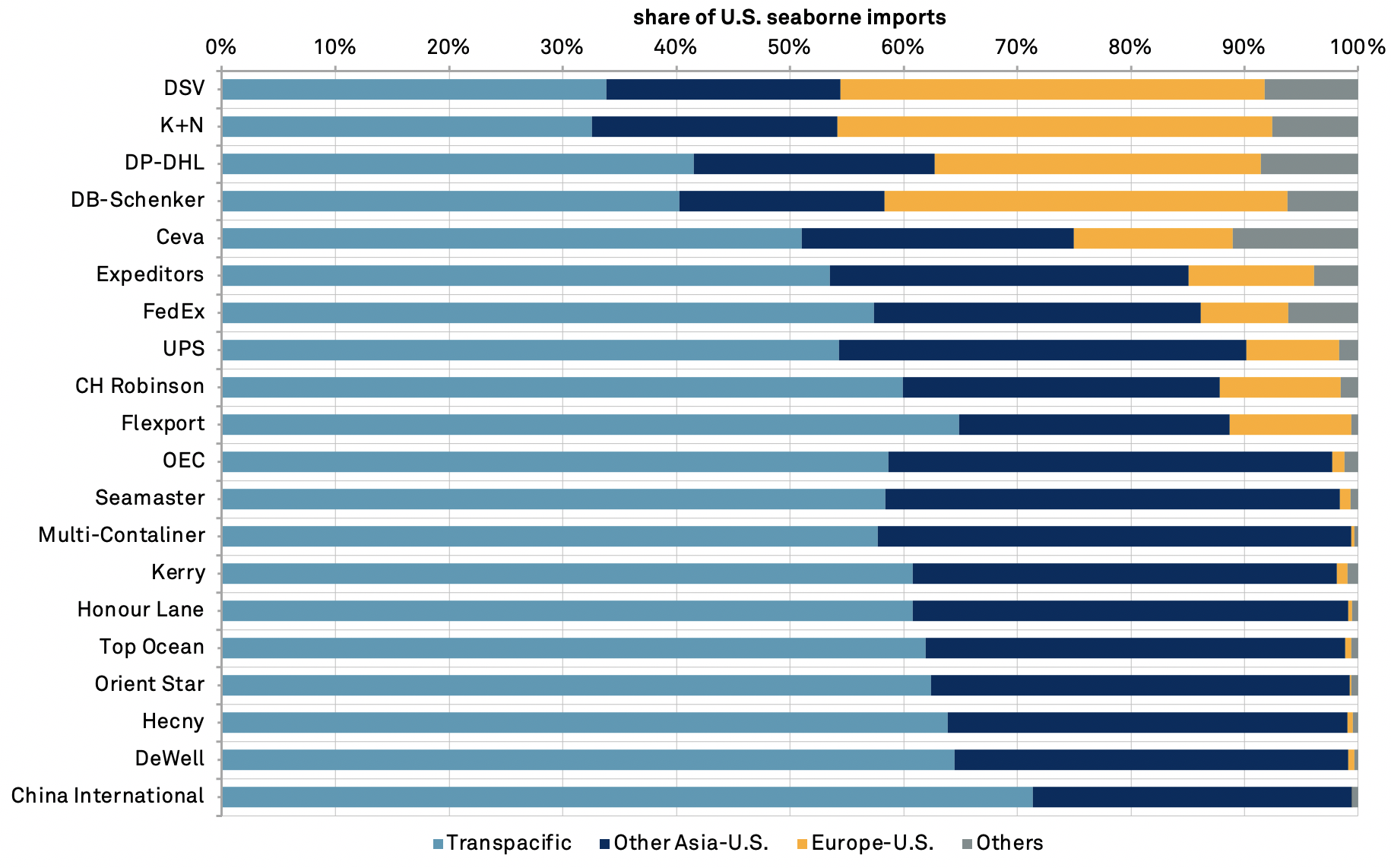

There may, however, be a response in terms of forwarders looking to ensure a more balanced portfolio of operations – a critical part of DSV’s strategy alongside the increase in scale. DSV already had the most diversified business by geography on U.S. seaborne routes in the 12 months to March 31, based on the standard deviation of shares by region.

Transpacific routes accounted for 33.8% of imports, while imports from Asia ex-Transpacific accounted for 20.6% and Europe 8.3%. The next closest were K+N and DP-DHL as a result of their exposure to shipments from Europe.

Source: Panjiva