Es

EsHapag Lloyd’s full year results statement and conference call (paywall) has confirmed their earlier optimistic-but-cautious outlook that freight rates should “increase moderately”, but that “continued discipline” is needed. That echoes comments also made recently by Evergreen, as discussed in Panjiva research of March 1.

The company saw the fastest rate growth on Europe/Middle East routes with a 9.0% growth in rates, though this came at the expense of a 4.4% fall in volumes handled in the fourth quarter compared to the third. The best performing route was Transpacific, where there was a 2.9% rise in rates and 6.1% rise in volumes handled – possibly reflecting Hanjin Shipping’s demise.

Source: Panjiva

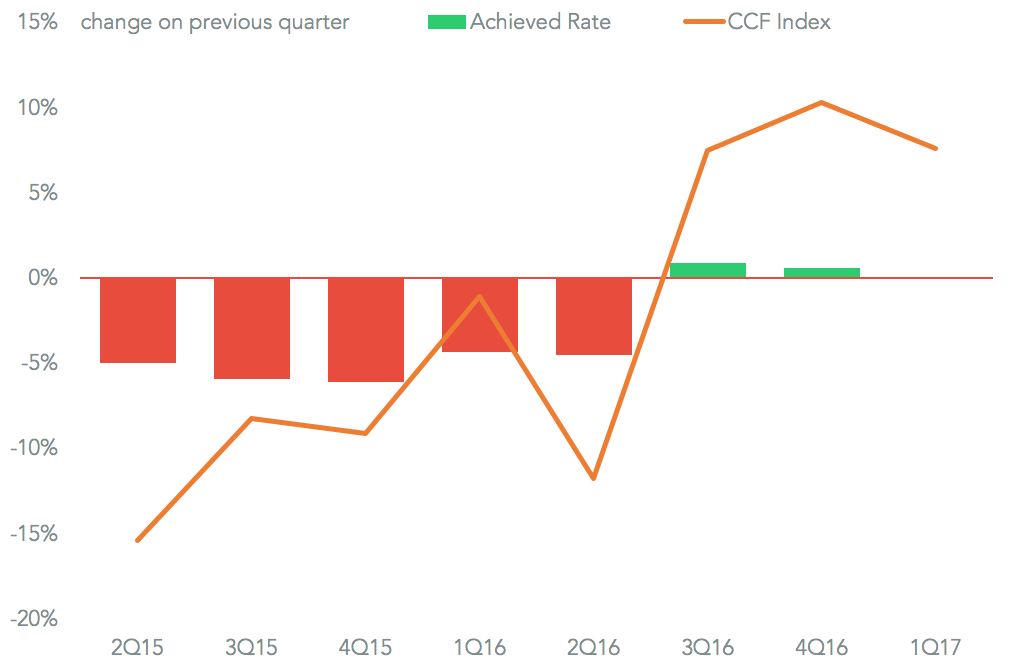

The company has indicated that it relies on long term contracts the repricing date for “the majority being April 1” on Asia-Europe rates and Transpacific routes being one to two months later than that. That process is confirmed by Hapag-Lloyd’s average achieved rates vs. market rates. Panjiva analysis of company financial statements and the Shanghai Shipping Exchange’s CCFI rate shows the effect of contracting mean the quarter-on-quarter movement on rates was less extreme than that in the market except for 1Q 2016. Yet a cumulative 25.3% rise in market rates in the past three quarters has only translated into a 1.5% rise in achieved rates. The seeds of a slowdown may have been sown already, however, as rates have fallen 11.4% since their mid-February peak.

Source: Panjiva