Es

EsThe freight forwarders operating on U.S.-inbound seaborne lanes had a fast start to 2018 as January shipment volumes surged 7.9% higher than a year earlier, Panjiva data. That was in large part the result of an increase in volumes from Asia, as outlined in Panjiva research of February 8, including a 10.3% increase in shipments from China, 15.2% from India and 13.3% from Vietnam.

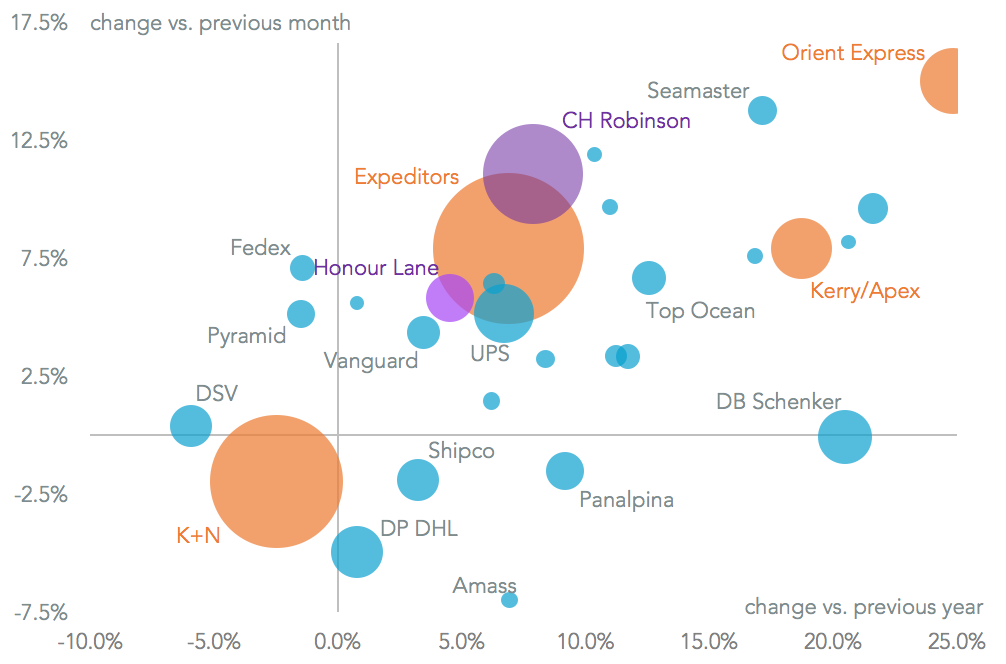

The Asia-centric nature of the improvement likely explains the outperformance of regional specialists. Orient Express saw the fastest growth among the top 20 shippers with a 24.8% increase in volumes vs. a year earlier, while Kerry’s Apex climbed 20.5%. By contrast the European specialists saw a slowdown including a 2.5% drop from Blue Anchor (K+N) and a 5.9% drop from DSV. The latter may be looking to preserve its margins after a solid fourth quarter performance. DB Schenker was the most aggressive of the European shippers with a 20.5% rise.

The U.S. domiciled operators do not yet appear to have made the tax-reform driven bid for increased market share that we had raised as a concern in our 2018 Outlook for sector profitability. The biggest three U.S. operators all increased volumes inline with the average including UPS (6.7%), Expeditors (6.9%) and CH Robinson (7.9%). UPS in particularly may be taking a more conservative approach after its challenging fourth quarter results.

Source: Panjiva

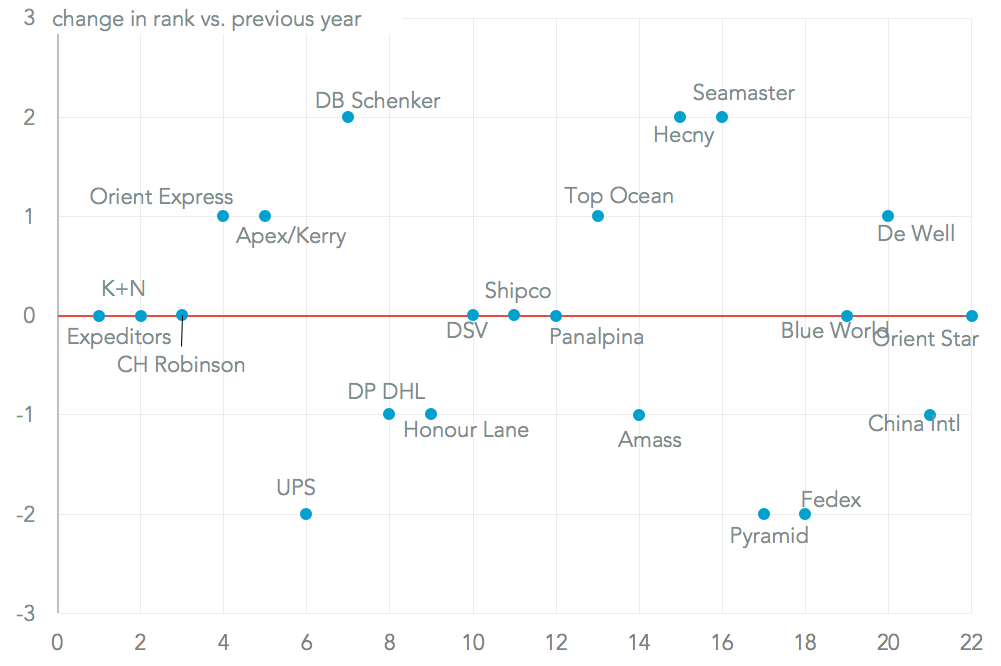

The aggressive bid for market share from Orient Express and Apex / Kerry meant both climbed up the rankings of operators to fourth and fifth respectively overtaking UPS (sixth from fourth a year earlier). Meanwhile DB Schenker outstripped both DP DHL and Honour Lane.

Source: Panjiva

The surge in Asian markets (and shippers) vs. Europe provides another spur to potential consolidation in the sector. So far K+N, DSV and Panalpina senior management have all referred in the past six months to wanting to participate in consolidation in the industry. The potential exit of CEVA’s shareholders may also figure in M&A calculations for those companies. That the top 10 operators only have a 16.4% share of shipments from 16.5% a year ago shows that the process of organic consolidation by competing for market share is not going anywhere.

A comparison of forwarder / port of lading mixes shows the gaps that Asian shippers (including Kerry, Honour Lane and Orient Express) could be easily filled with European shippers’ coverage (including K+N, DB Schenker, DP DHL and Panalpina). Whether the financial aspects of such deals can be made to make sense is a different matter of course, and something that will likely be a focus in the aftermath of the ongoing fourth quarter earnings reporting season.

Source: Panjiva