Es

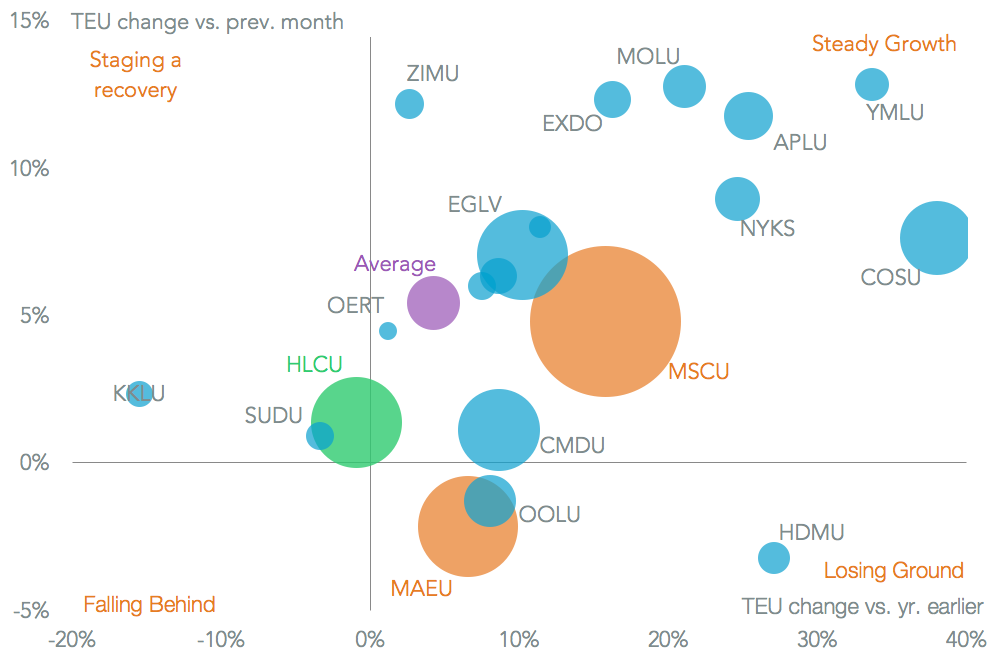

EsContainer-lines operating on U.S.-inbound routes had a strong performance as a group in July, with a 4.2% increase in containers handled, Panjiva data shows. Growth was principally driven by shipments from China and Asia (particularly Vietnam), as outlined in Panjiva research of August 7, as reflected in the stronger-than-average performance of the Asian shippers.

COSCO Shipping, which was also helped by the consolidation of CSCL a year earlier, was the fastest growing of the large shippers with a 38.4% growth. Meanwhile two of the three Japanese shippers saw growth of over 20% (NYK and Mitsui-OSK) suggesting the growth seen in the second quarter will continue.

Source: Panjiva

Notably MSC, which has not partaken in the current round of M&A, also increased its market share after growing volume by 15.8%, increasing its market share to 9.27% from 8.1% a year earlier.

The only significant loser during the month was Hapag-Lloyd, which saw its volumes drop 0.9%, and its market share for the past three months fall by 0.24% points compared to a year earlier to reach 5.57% (5.82% including). That may reflect challenges it is facing while completing its merger with UASC. If it does, then the other shippers going through mergers or acquisitions – ONE, Maersk and COSCO Shipping – may see problems at a later stage.

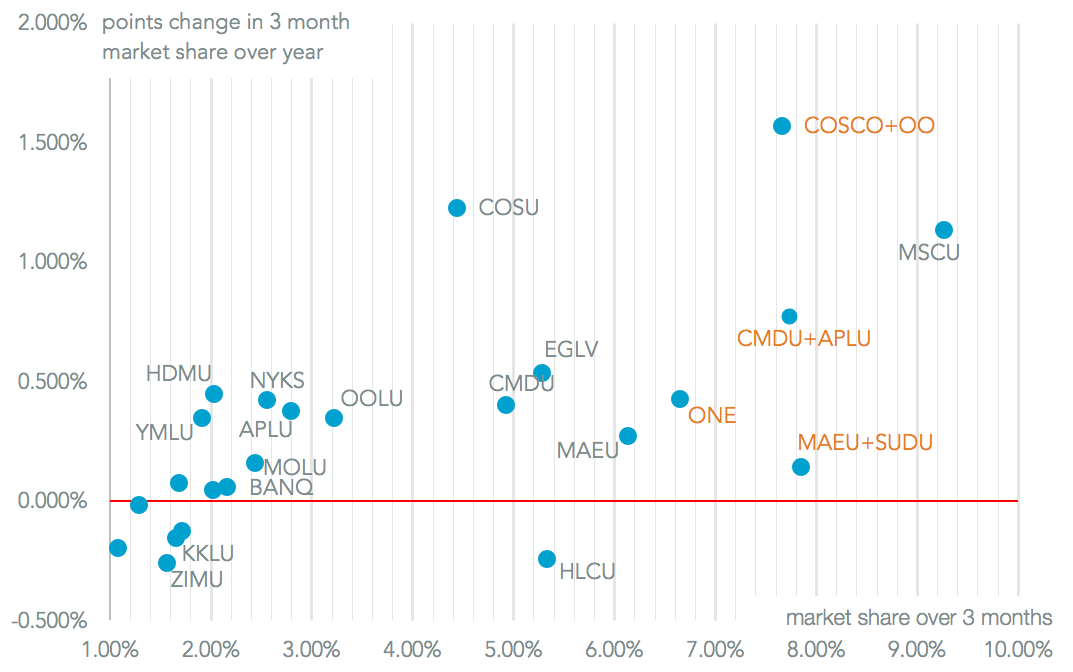

The larger shippers continue to take market share from the smaller ones, even not allowing for the mergers. The top 10 “post merger” liners would have held a 56.0% market share, up 4.87% points on a year earlier.

Source: Panjiva

That process is by no means guaranteed of course. Of particular concern are regulatory approvals for COSCO Shipping’s bid for Orient Overseas. Panjiva analysis of nearly 4,400 carrier-country pairs shows the new entity will be a top 3 shipper on at least eight U.S. inbound lanes vs. four for the two separately. That includes China, Hong Kong, Vietnam, Malaysia and Canada.

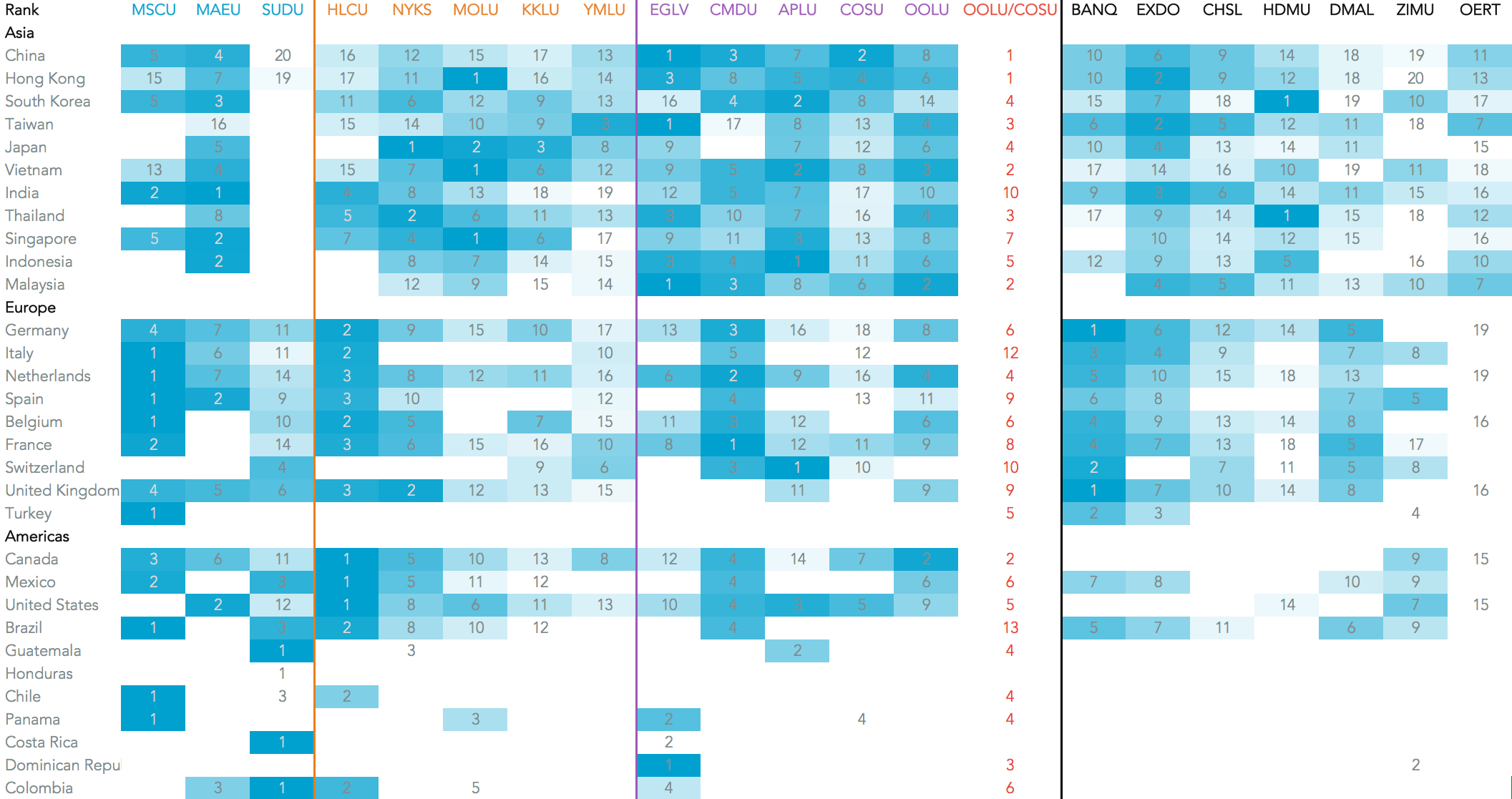

Putting aside the large NVOCCs the remaining players that are not already in an alliance are Hyundai Merchant Marine – which is tying up with other South Korean shippers – and ZIM, which has a vessel-sharing arrangement with the 2M alliance.

Source: Panjiva