Es

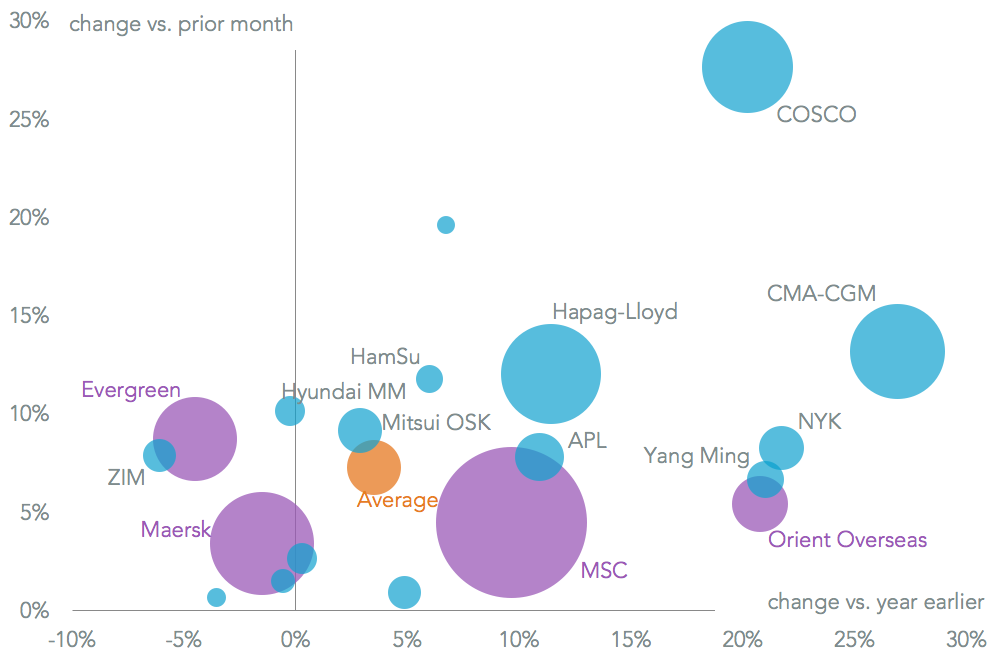

EsContainer-lines operating on U.S.-inbound routes saw a 3.5% growth in handling in October vs. a year earlier, Panjiva data shows. Only a handful of the top 20 operators saw a drop in handling. Maersk saw a reduction of 1.5%, which may reflect it attempting to improve margins after the recent third quarter results that saw a drop in profitability, as outlined in Panjiva research of November 8.

Privately owned MSC may not be so constrained, with a remarkable 9.7% growth in handling considering it is already the largest operator. Among the Asian shippers Evergreen lost out, with a 4.5% slide in handling. It may have lost out to Orient Overseas, which increased volumes by 20.8% despite the regulatory risks presented by the review of its takeover by COSCO Shipping.

Source: Panjiva

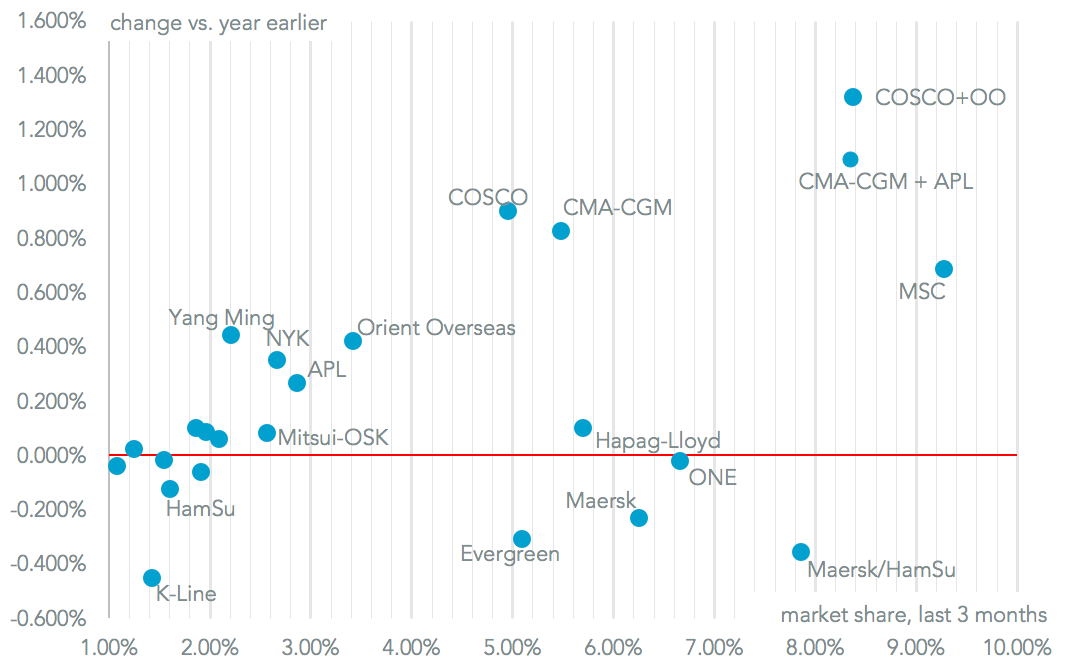

As a result of Orient’s growth, if the current round of consolidation in the sector was completed right now, COSCO/Orient Overseas would be the number two player with a 8.4% market share. That would put it ahead of CMA-CGM (8.3% despite a 1.1% point market share growth) and Maersk/Hamburg Sud (7.9% market share, down 0.4% points). The emergence of the new top tier raises questions for Hapag-Lloyd (5.7%) and Evergreen (5.1%) strategically.

Source: Panjiva

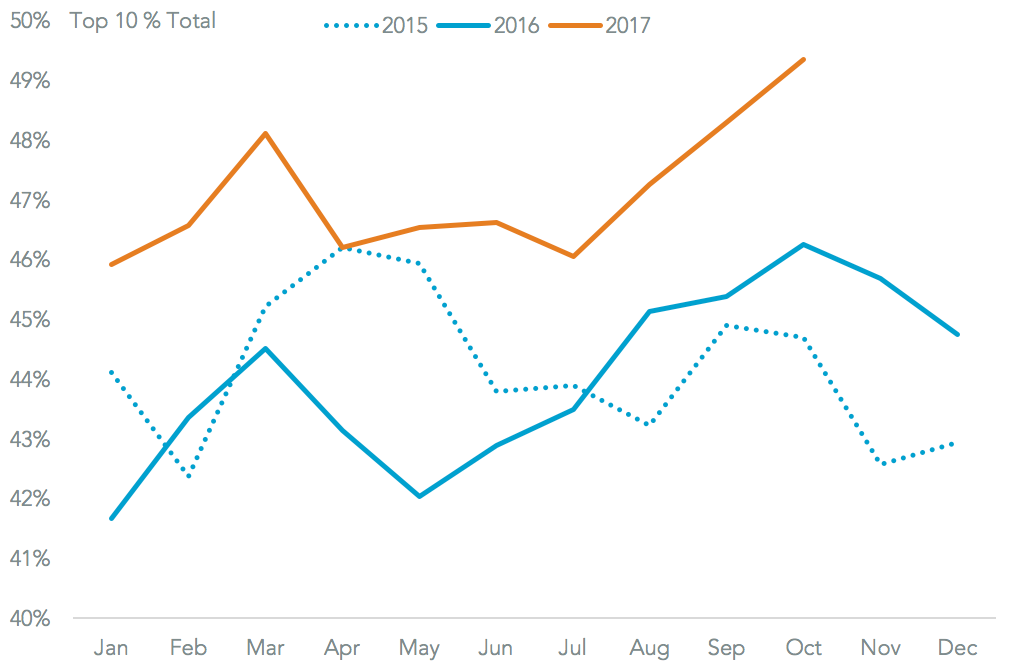

The biggest losers though have been the smaller operators below the top 20, which are steadily getting squeezed out of the market. The share of the top 10 in total shipments reached 49.3% in October, the highest on record and 3.1% points above a year earlier. The process of organic consolidation may make further mergers and acquisitions unnecessary, at least until Maersk’s purchase of Hamburg Sud and COSCO Shipping of Orient Overseas is complete.

Source: Panjiva