Es

EsPanjiva Research took part in a webinar on July 1 with our colleagues from S&P Global Market Intelligence and S&P Global Ratings to look at the use of supply chain data in the credit analytics process during COVID-19. A recording and content from the event can be found here while this report addresses some of the key questions asked.

Panjiva’s analysis, outlined in our June 17 report, has found that the consumer discretionary sector, and specifically the apparel and autos sectors, have seen the fastest downturn in U.S. seaborne imports in May and have yet to recover in June. Similarly S&P Global Ratings finds that, as of May 31, the consumer discretionary sectors and specifically cosmetics and durables, have the most negative outlooks and watch negatives.

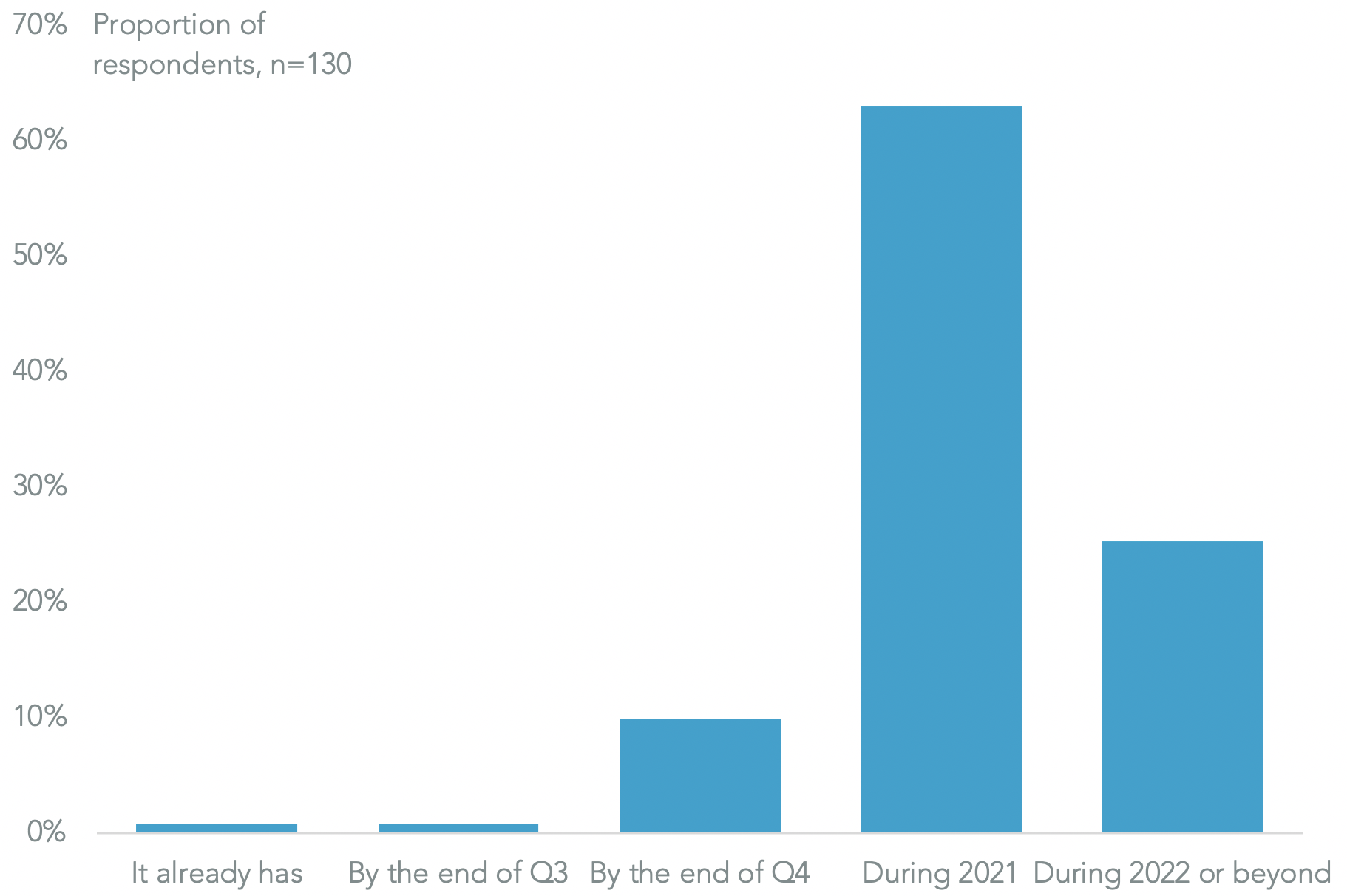

We asked the participants of the webinar, drawn mostly from the credit financial community and credit divisions of non-financial corporates, “How long will it take for supply chain activity to return to pre-pandemic levels?” By far the majority don’t see a return to normality in 2020 with 63.1% of respondents expecting it during 2021 and a further 25.4% not expecting it until 2022. That aligns with S&P Global Ratings‘ macroeconomic outlook for global GDP.

Source: Panjiva

Q: If there’s another surge in cases sufficient to lead to another round of industrial lockdowns, what might the impact be?

From a credit rating perspective a new surge will have a particularly strong impact on companies currently in the ‘B’ and ‘CCC’ rating category which have little room left in their balance sheets to weather a further loss of business. Firms in apparel and travel services will be particularly vulnerable. There may well be further defaults. Investment grade firms should do better given their extra balance sheet capacity.

In terms of supply chain impact there could be a marked knock-on effect for upstream suppliers to the consumer discretionary sector with a seasonal element including apparel and leisure goods such as toys. We’ve already seen a significant impact on suppliers in Bangladesh and Cambodia from orders cancellations by U.S. retailers.

Q: Could central and eastern Europe emerge as a winner from supply chain diversification?

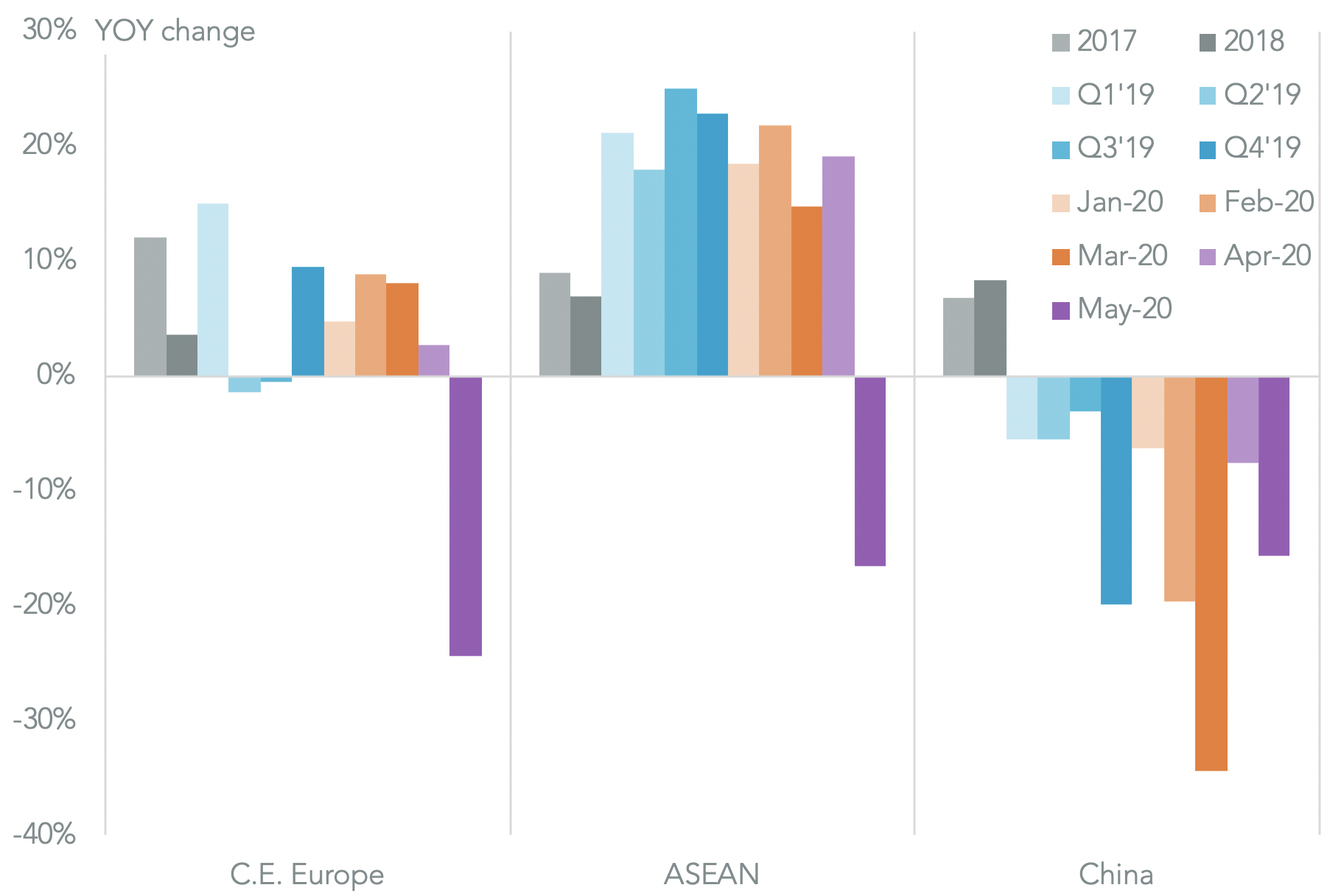

CEE countries that are in the EU could benefit from the shift to “in market for market” strategies with shortening of supply chains in response to COVID-19. Exporters of pharmaceuticals from the Czech Republic may be well placed in particular. Those outside the EU will have to rely on competing with emerging markets, particularly in Asia, for “China + N” strategies.

Panjiva’s U.S. seaborne data shows that shipments from CEE countries ( OECD definition) have increased by 0.6% in the six months to May 31 while those from south-east Asia ( ASEAN) have increased by 12.6% and shipments from China dropped by 17.5%. In 2019 compared to 2017 – a proxy for the U.S.-China trade war – shipments from CEE have increased by 8.7% while those from SEA have surged 30.3% and imports from China dropped 1.3%.

Source: Panjiva