Es

EsShippers made plenty of positive comments about rates during their quarterly conference calls, but the rates themselves didn’t bear this out in February. The CCFI container index fell 7% in the month, partly due to the lunar new year holiday early in the month, though a 13% drop in Europe-bound routes led the declines. Further volatility is likely as the new alliances (THE and Ocean) get started in April. Bulk rates diverged, with the Baltic Dry Index rising 7% on stronger commodity prices while tanker rates continued to slide despite oil prices inching ahead. The outlook for container a...

Related Research

Supply Chain Edge: Revealing rates, costing conflict, building artificial intelligence

– The resumption of US trade data after the government shutdown reveals new details about the rates of tariffs being paid — the h... Read more →

Supply Chain Edge: Tariff smoke clearing, Tesla’s energy duties, front-loading for 2026

Key findings – The past week has brought more details on US International Emergency Economic Powers Act (IEEPA) tariffs and relat... Read more →

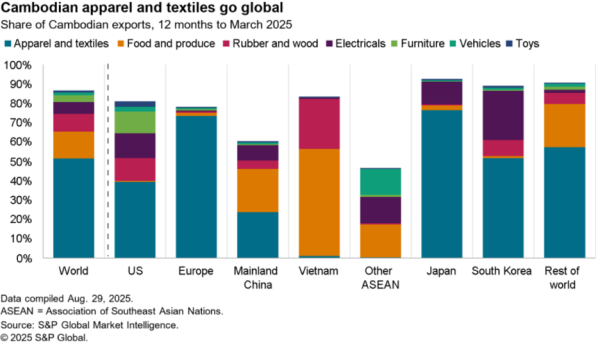

Supply Chain Edge: Focus on Cambodia, tariffs in Mexico, semiconductor charge

– Cambodia has emerged as a key reshoring center for apparel, with exports in this sector making up 45% of its total exports in t... Read more →

Supply Chain Edge: Reshoring’s future, chocolate’s choices and Türkiye’s wildfires

• In a new research series, we consider the future for reshoring in the wake of US tariffs and ahead of forthcoming free trade de... Read more →

Copyright © 2025 Panjiva Supply Chain Intelligence, a product offering from S&P Global Market Intelligence Inc. All rights reserved.