Es

EsAs of Sept. 3 there are just 18 Parliamentary session days to address the risk of a no-deal Brexit, the BBC reports.

In reality that may be as few as six given: uncertainties around the date of Parliamentary suspension; the need for Prime Minister Boris Johnson to agree a new deal with heads of state at an EU Council meeting on Oct. 17 and; the Prime Minister’s commitment that “there are no circumstances” under which he would request a Brexit delay, according to The Guardian.

As flagged in Panjiva’s research of Aug. 29 trade policy – including Brexit as well as tariffs resulting from the U.S.-China trade war and other disputes – has become an increasing preoccupation for corporations globally.

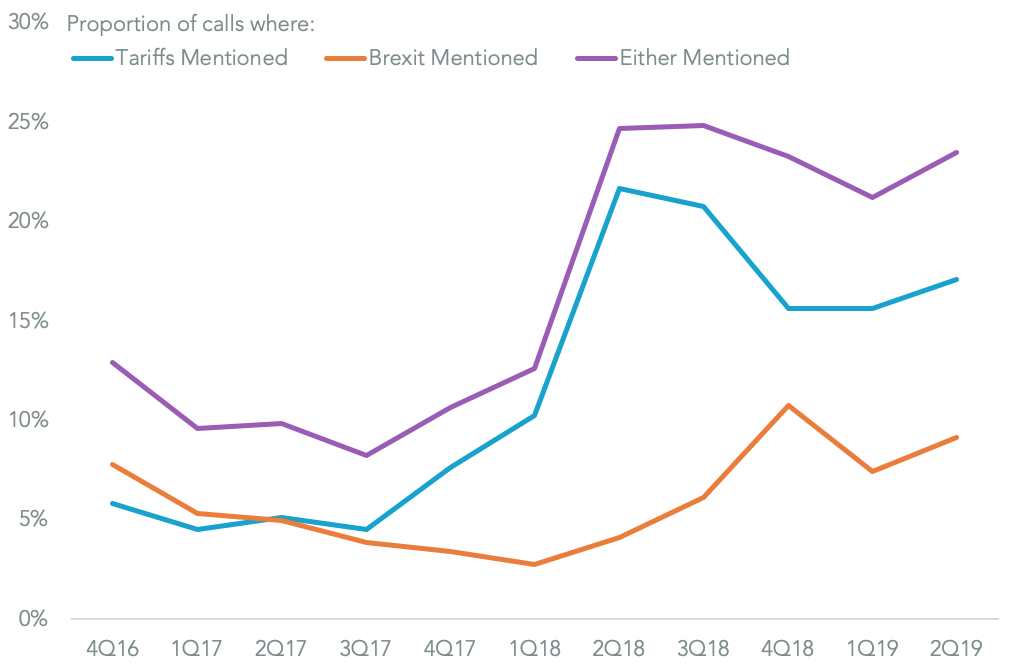

In the 2Q reporting season through Aug. 28 9.1% of company transcripts across Europe and the U.S. – captured by S&P Global Market Intelligence – mentioned Brexit, up from 7.5% the prior quarter but below 10.8% peak recorded in the Jan. 1 to March 31 period. That compares to 17.1% of calls that mentioned tariffs more broadly.

Source: Panjiva

Looking specifically at the period since the initial Brexit deadline – and to capture companies on semi-annual reporting – Panjiva’s analysis of over 15,000 transcripts from across European and North American companies shows 8.3% have mentioned Brexit. Geographically British-quoted companies obviously have the highest ratio at 38.7%.

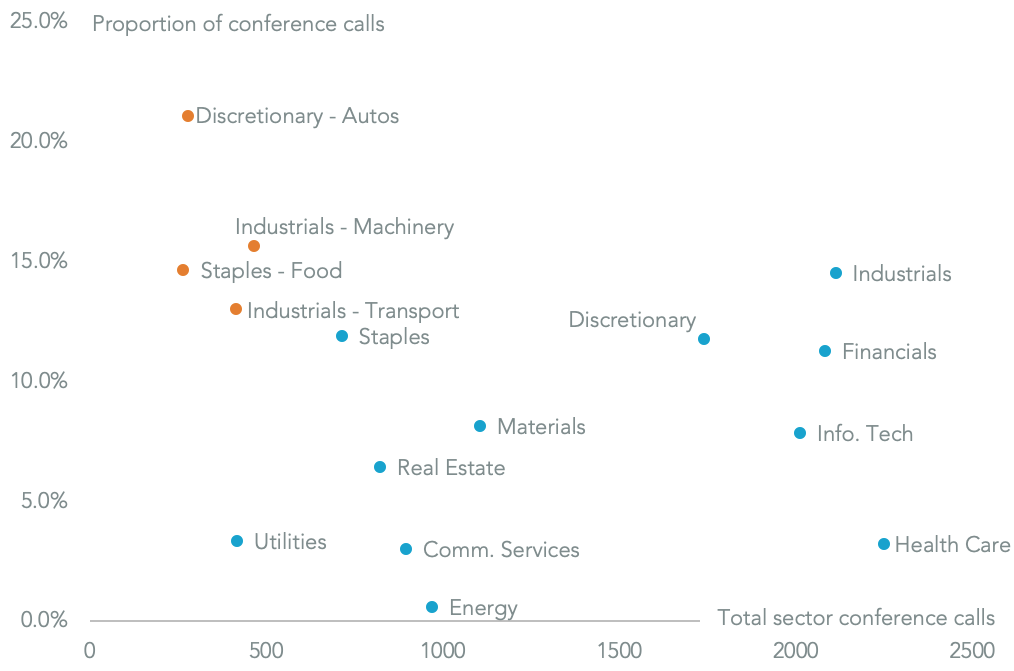

At the industry level 21.1% of all automotive firms, 15.7% of machinery manufacturers and 14.7% of food manufacturers have discussed the topic across all countries. The transportation sector also evidently has a significant exposure with 13.0% of companies having Brexit discussed in their calls.

Source: Panjiva

A review of transcripts in the capital goods and automotive sectors suggests that many companies have built preemptive stockpiles and expect a slowdown in the economy, but that there is little certainty as to what the effect of a no-deal Brexit on day-to-day operations will be. For example:

– Aston Martin Lagonda CEO Andrew Palmer stated that the firm is already carrying extra inventories from the run-up to the original Mar. 31 data for Brexit and that will be “sufficient to see us through what may be a disorderly Brexit“.

– Cummins CFO Mark Smith has stated that the firm has “concerns around logistics, freedom of movement of goods, concern about bureaucratic delays” while the firm has “maintained” some additional inventories in the short-term.

– Delphi CEO Richard Dauch has cut the firm’s outlook and now expects “full year production in Europe to decline by approximately 3%, or 1% lower than our prior view, primarily due to uncertainty related to Brexit and revised GDP forecasts”.

– Electrocomponents CFO David Egan stated that as much an inventory increase of as much as 1.2% points of revenues “relates to inventory we brought in off the back of Brexit planning” in the most recent financial quarter.

– Jaguar Land Rover CEO Ralf Speth noted that the firm “lost about GBP 100 million in the quarter on Brexit” due to a shut-down in April planned to coincide with the original Brexit date. Speth has also said that planning for a no-deal Brexit will mean the firm “will build stocks where (it) can“. Longer-term Speth has stated he “would expect friction, exactly how much, I don’t think anybody is in a position to actually say“

– Spirax Sarco CFO Kevin Boyd stated that the firm’s lower operating cash conversion in the latest quarter has been a “result of an increase in working capital due in part to planning for Brexit“. Looking ahead Boyd also noted “Brexit is sure to have an impact, but we’ve not tried to forecast it“.

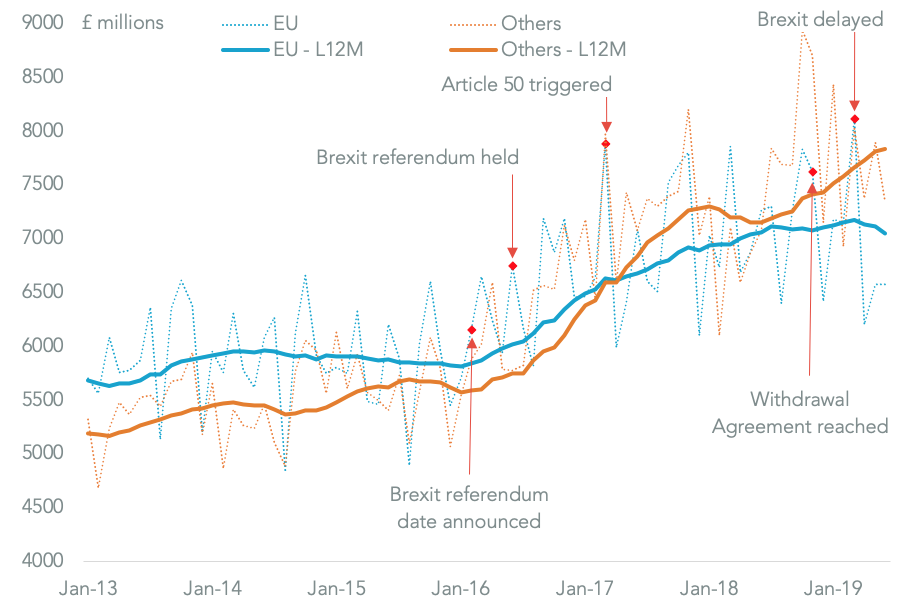

Panjiva analysis of official data shows there are already signs of manufacturers cutting back imports of intermediate machinery and electronics from the EU in response to Brexit. Over the longer-term imports from the EU dropped to 47.4% of a total £178.7 billion ($215.6 billion) in the 12 months to Jun. 30 versus 50.9% in 2015.

Source: Panjiva

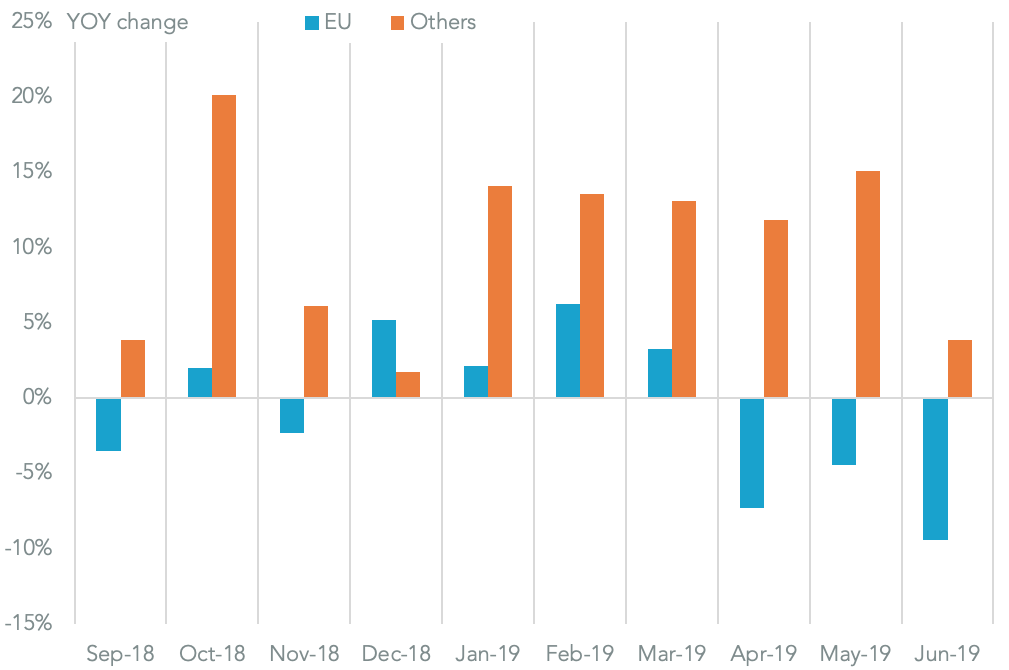

In shorter term the hangover from earlier inventory build can be seen. There was a 9.4% year over year drop in imports of intermediates machinery and electronics from the EU in June, bringing the 2Q reduction to 7.1% after a 3.8% rise in 1Q. By contrast imports from non-EU suppliers rose 10.2% in 2Q after a 13.6% surge in 1Q.

Source: Panjiva