Es

EsNAFTA negotiations re-open this weekend, and for once the tough issues are being dealt with upfront – we take a look at the agricultural aspects of talks. In logistics, Seattle and Tacoma have had a tough start to 2018 and Matson’s 4Q results show just how different it is to other liners. Also: Beijing Auto isn’t worried about NAFTA, it’s planning a Mexican factory; India’s new industrial solvent tariff; a new investigation of Chinese rubber band exports; the EC isn’t pursuing a hand-truck circumvention case; Secretary Ross’s comments on a “thoughtful” approach to metals tariffs; the USTR has delayed its annual section 301 review hearing; India and Canada will continue trade talks; and Indonesia has postponed new shipping rules.

Daily Datum: $578 million

Chinese exports of cars to Mexico in 2017

NEED TO KNOW

NAFTA Watch: Agri-vation, Metal Mayhem to Join Origin-al Problems as Round 7 Looms

The seventh round of NAFTA negotiations from February 25 appear set to begin with the difficult issues of automotive rules of origin and agricultural market access. Mexico will want to leverage its position as a buyer of $12.1 billion of American basic foodstuffs in 2017, or 75% of its total of those products. The largest areas of exposure for U.S. farmers include corn ($2.7 billion of sales, where Brazil is already competing), soybeans ($1.6 billion, both Brazil and Paraguay can compete) and pork ($1.3 billion).

The bigger controversy is access to Canada’s dairy sector. While American dairy exports globally climbed 12% in 2017 (following a prolonged downturn) those to Canada fell 7% and accounted for just 8% of the total.

The Canadian government may also raise the recent tariff decisions in solar panels, and forthcoming aluminum and steel “section 232” reviews by the U.S. as issues. It supplied 26% of U.S. imports of the steel and aluminum products being investigated in 2017. Other potential sticking points will likely include dispute settlement and government procurement. The latter should provide clarity on whether Canada’s hawkish rhetoric recently will be translated into a hardening of its negotiating stance.

Read more →

Source: Panjiva

SeaTac’s Tough 2018 Start May Get Tougher as Shippers Consolidate

Container handling through the Puget Sound ports of Seattle and Tacoma fell 17% on a year earlier in January, the fourth straight month of declines and the worst monthly performance since March 2016. Loaded imports dropped 25%, underperforming an 18% slide in exports (empty container handling improved) while intra-U.S. handling to Hawaii and Alaska also declined.

Traffic from China was the main culprit, with a 23% slump to 90,000 TEUs being the worst January performance in at least 10 years. The port authority has cited changes in shipping alliances as one cause for the decline. Shipments by Maersk fell 28% on a year earlier, while those by ZIM slumped by 81%.

The ports also faces a challenging 2018 due to container-line consolidation presenting it with larger customers that have more negotiating clout. Currently CMA-CGM is the larger shipper with a 15% market share in the past three months. It will be overhauled by COSCO (16%) and ONE (17%), at which point the top five shippers will account for 70% of volumes.

Read more →

Source: Panjiva

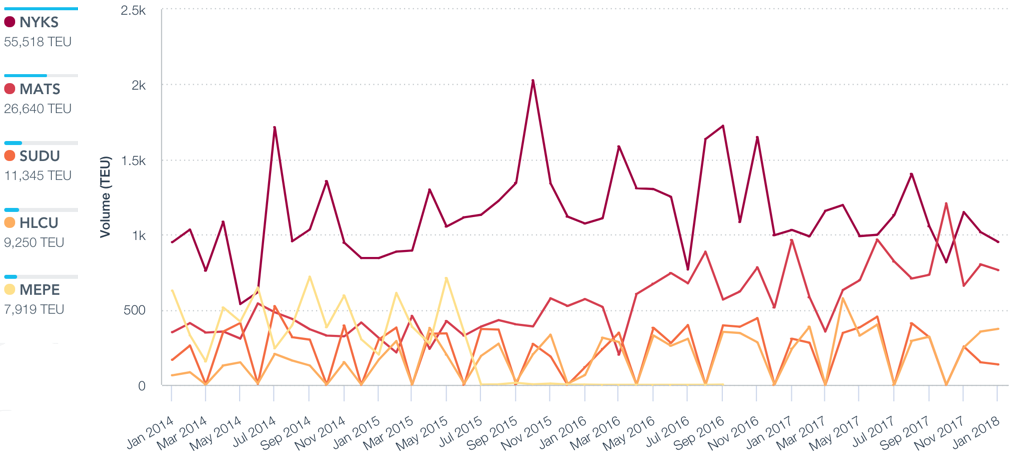

Matson Slips as Container-Lines Soar, Jones Act May Prove a Hinderance

Container-line Matson reported 4Q 2017 revenues that fell 1% on a year earlier, though that was 2% better than expected. The downturn was due to an 11% slump in Hawaiian traffic which has shown no sign of recovering in 2018 based on NWSA data. The better-than-expected revenues may reflect premium pricing in its Chinese service, though volumes there have fallen too. The decline in revenues compares to a 15% improvement for the container-line sector broadly.

The company expects rates, but not volumes, to improve in 2018 though it continues to face stiff competition. Matson’s share of Hawaiian incoming traffic ex U.S. dropped to 31% from 36% a year earlier in January. The company still has best-in-class profitability at 12% on an EBITDA basis due to Jones Act protected status on intra-U.S. traffic. Yet, that was down 15% on a year earlier and its Jones Act status may prevent it from seeking strategic alliances with other major shippers into Hawaii including Hapag-Lloyd and ONE.

Read more →

Source: Panjiva

GLOBAL TRADE WRAP

Coming back to NAFTA, many automakers appear unconcerned about the new rules. Beijing Auto (BAIC) has committed $1 billion to a new car factory in Mexico that will open in 2020, despite uncertainty on tariff rules within the region. Under current regulations Chinese automakers appear to be doing well. Exports to Mexico reaching $578 million in 2017 and an annual run-rate of 2.5x that in the last two months of the year. (Panjiva Research – Industries)

The Indian government has launched a slew of “Make in India” tariffs in 2018 already, though mainstream trade cases continue too. The government will apply duties to Chinese exports of the industrial solventdimethylacetamide. So far the case, which started last March, has not scared producers off with shipments having fallen by just 9% in the fourth quarter on a year earlier. It remains to be seen whether the $211 / ton duties will be sufficient to change that. (Panjiva Research – Industries)

The U.S. Commerce Department will take up an investigation of Chinese rubber band exports. That isn’t a surprise given it has taken up every case petitioned since the start of the Trump administration. There appears to be a clear case to make though with Chinese exports to the U.S. having bounced 29% higher in the fourth quarter on a year earlier. (Panjiva Research – Industries)

A third investigation of Chinese exports comes from the European Commission, though in this instance the EC decided to not investigate circumvention of hand truck duties. The case alleged Vietnamese exports to the EU were simply constructed from all-Chinese parts. The EC did not agree from a threshold perspective. Meanwhile Chinese exports directly to the EU climbed 20% higher in 2017 vs. 2016. It may be the U.S. that needs to launch a dumping case though after exports surged 34% over the same period. (Panjiva Research – Industries)

The biggest outstanding trade case right now is the American section 232 review of aluminum and steel. While the recommendations to President Trump were announced late last week, as discussed in our 2/19 report, a decision has yet to be made. Commerce Secretary Ross has stated that he is sure the President will act “in a very thoughtful and systematic way,” but has “no idea” when a decision will be made (there’s an April 11deadline for steel). At the same time Defense Secretary Mattis has said “targeted tariffs are more preferable than a global quota or a global tariff” in reference to the impact on American relations with its allies. (CNBC, Bloomberg)

The USTR has delayed a public hearing of comments in its annual section 301 review of intellectual property practices globally. It will now be held on March 8 not February 27. While it is a complex review, the delay may be a sign that the separate, specific review of China – outlined in our 2/07 research– may be close to reaching a conclusion. (Federal Register)

The governments of India and Canada have agreed to continue their negotiations of the Comprehensive Economic Partnership Agreement, in a meeting between Prime Minister Modi and Prime Minister Trudeau. That’s a better outcome than we had feared in our 2/16 analysis, but comes with few details. A key sticking point is likely to be the Canadian government’s preference for wide ranging deals, as well as the short-term imposition of a wide range of tariffs by the Indian government under the “Make in India” banner. (Prime Minister’s Office)

The Indonesian government has postponed plans requiring the use of domestic vessels for the export of palm oil and coal. As discussed in our 2/09 research that would have put access to the fast growing Chinese market for palm oil, which grew 29% in 2017, at risk. The losers from the delay are Malaysian suppliers, the second largest after those from Indonesia. The regulations could yet be implemented, however. (S&P Global Platts)