Es

EsCarriers continued to enjoy the high prices plaguing shippers in recent months. Freight rates increased by 1.2% week over week on Dec. 10, based on the Shanghai Shipping Exchange index. This puts rates from China to the U.S. West Coast up 23.8% since the end of July and 96.4% since the end of 2020, eliminating any thought that November represented the peak of rates. For shippers, the price hike represents additional supply chain costs, and comes as both carriers and shippers start to think about contract rates for next year. If rates show no signs of decreasing, shippers may find it harder to argue for more downside flexibility in 2022.

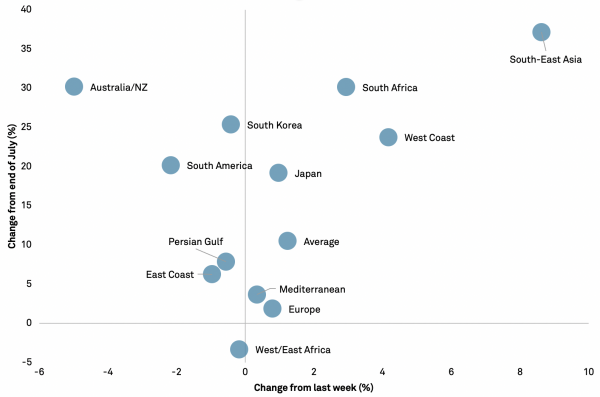

Other routes with notable changes include China to South Asia, likely in direct competition with Pacific routes, and carriage to South Africa, where the omicron variant was first discovered. These routes were up 8.6% and 2.9% respectively over the past week and show increases of 37.5% and 30.2% since the end of July. Shippers from China to the U.S. East Coast may find some relief as rates dipped 1.0% over the last week. This strengthens the competitiveness of Panama Canal crossing routes that traditionally take more time but are now offset by extreme lead times through the ports of Los Angeles and Long Beach.

Data: Shanghai Shipping Exchange Source: Panjiva

Carriers tend to benefit the most from high shipping rates, but not all of them show the same performance. There may be negative pressure on rates when holiday shipments wane, as carriers look to regain market share. In November, MSC and ZIM continued to lead 2M to a 6.3% increase year over year in import activity, the highest among the three alliances. Panjiva data shows that imports associated with MSC rose by 14.3% and those with ZIM increased by 21.7%, offsetting the 4.6% decline in volumes handled by Maersk.

CMA CGM posted a 14.3% year-over-year rise, although that pulled the Ocean Alliance only up to growth of 3.5%. Nevertheless, CMA CGM and COSCO recorded positive import momentum during the month, with growth rates increasing by 6.5 percentage points for CMA CGM versus the three months to Nov. 30 and by 8.4 percentage points for COSCO in the same period. This could indicate that the shipments handled by those carriers were delayed, if not more competitive.

Unaffiliated carriers SM Line and Matson continued to show increased activity in November. Imports associated with SM line were up by 58.0% year over year during the month and by 20.7% in the three months to Nov. 30. Imports linked to Matson grew only by 5.9% from the previous year after a strong October, possibly signifying weaker momentum.

Source: Panjiva

Forwarders are likely in a less advantageous position, stuck in between the carriers and shippers. Regardless, imports associated with Ceva Logistics, Amazon and Multi Container in November all increased from the comparable period last year. Imports linked to Ceva grew by 95.8%, the highest among forwarders, while Amazon was close behind with volumes up by 88.1%. Amazon’s success may be driven by the integration of its logistics practice and e-commerce arm, a factor that has raised concerns from regulators. Meanwhile, volumes handled by Multi Container increased by 50.7%. This growth may also be partly driven by delayed orders coming in against favorable comparisons, but it still shows that the forwarder market remains dynamic.

Source: Panjiva