Es

EsThe White House will apply 10% duties on all products not already covered by tariffs from Sept. 1. President Donald Trump cites a lack of delivery on agricultural purchases and talks more generally earlier in the week. The implementation has been delayed as the U.S. Trade Representative is still consulting on whether the so-called “list 4” tariffs should include all, or a subset, of products.

It’s not yet clear what China retaliation may be but it will likely be non-tariff in nature. The government may decide there is no point in negotiating. Active measures could include reduced purchases – including of agricultural products by state-owned enterprises – implementation of the unreliable entities list discussed in Panjiva research of Jul. 31, or regulatory measures such as customs and enforcement actions.

Importantly – as was the case ahead of list 3 tariffs applied in December last year – they’ll likely be a surge in imports right at the start of the peak shipping season as companies seek to preempt tariffs.

Panjiva analysis shows that the biggest products not yet covered are all in the consumer sector and include: smartphones where imports were $43.2 billion in 2018, representing 81.8% of total imports; apparel and footwear worth $42.1 billion, representing 37.6% of the total; laptop PCs worth $37.5 billion, equivalent to 94.4% of the total; toys worth $11.9 billion which is 97.6% of the total; and videogame consoles worth $5.4 billion, representing 97.6% of the total.

Imports of toys and videogames peak in October, Panjiva data shows. Tariffs on toys seem to be unwise politically ahead of the holidays. Hasbro has already indicated that switching supply chains is slow and takes years to implement.

Laptops have a double peak in shipments in August for back-to-school sales and November depending on model release schedules. There could be an acceleration in shipments of higher end models by shipping by air rather than sea, though will be a function of whether margin makes it worthwhile.

Both Dell and HP are already planning to move production out of China for the longer term. China accounted for 88.7% of Dell’s U.S. seaborne imports in the 12 months to Jun. 30. HP Inc. meanwhile, supplied by Quanta, still sources 100% of its laptops from China.

Source: Panjiva

The largest group overall is smartphones with $43.2 billion imported in 2018, representing 81.8% of the total. Imports are seasonal with the peak typically in November as a result of Apple’s product release cycle. That comes as growth slowed to 3.5% in dollar terms in the 12 months to May 31. That there was growth is down to increased values per phone given the number of phones fell 1.9% over the same period.

There’s already evidence of stockpiling. Imports in May alone surged 24.3% higher year over year in handset numbers and by 26.3% in dollar terms. There may have been the result of a breakdown in the earlier round of talks that brought increases in list 3 tariffs to 25% from 10% as well as threats regarding list 4 tariffs.

Source: Panjiva

Given phones are largely a luxury good with complex supply chains many manufacturers may simply increase prices rather than retool their manufacturing.

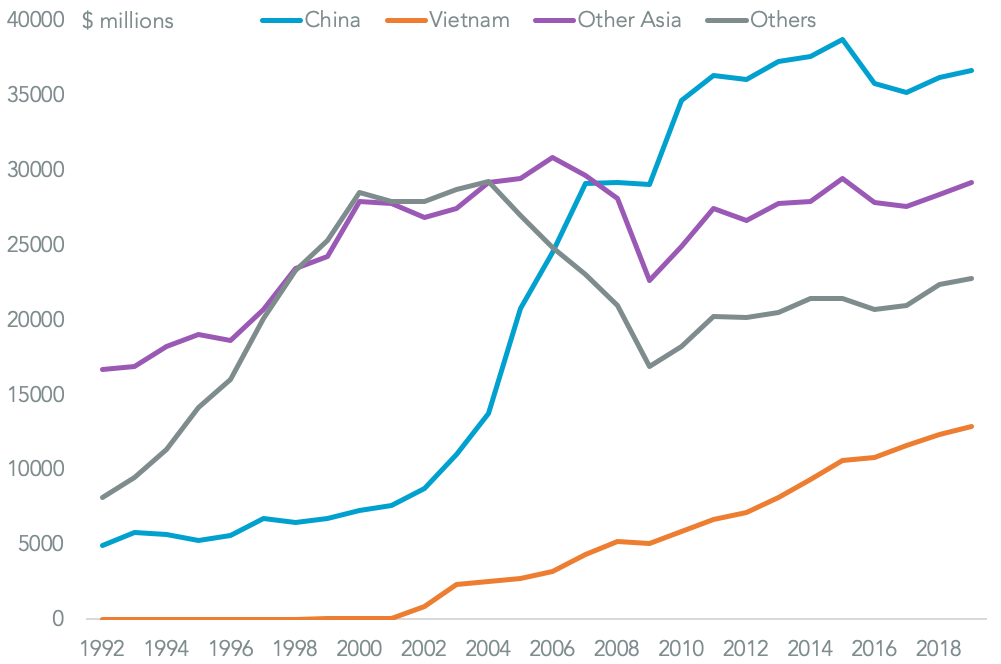

Yet at the other end of the spectrum tariffs may lead to price increases of apparel and footwear. Imports from China have already fallen to 37.6% of the total following nearly two decades of shifting production. Yet, it’s still the largest production center with Vietnam representing 16.8% and other Asian countries 22.5%.

Apparel makers including Ralph Lauren and Guess have already indicated a mixture of price increases and longer-term sourcing decisions will be used, Meanwhile the footwear industry including Adidas and Under Armour has stated in a combined notice in May that tariffs will be “catastrophic for our consumers, our companies, and the American economy as a whole“.

Source: Panjiva