Es

EsContainer-line Maersk is one of nine founding firms in the new “Transform to Net Zero” environmental initiative to cut greenhouse gas emissions to a net zero by 2050. The group is drawn from a variety of industries and includes manufacturers as well as services firms.

A shift to reduced GHG emissions by the shipping industry has been inevitable for some time, as discussed in Panjiva’s research of Jan. 20. In the near-term the European Parliament has also voted to include shipping in the Emissions Trading Scheme.

The inclusion of increased environmental costs for the shipping industry before mitigation through technological advancements – such as hybrid boats and alternative drive systems such as LNG – might be passed through to customers.

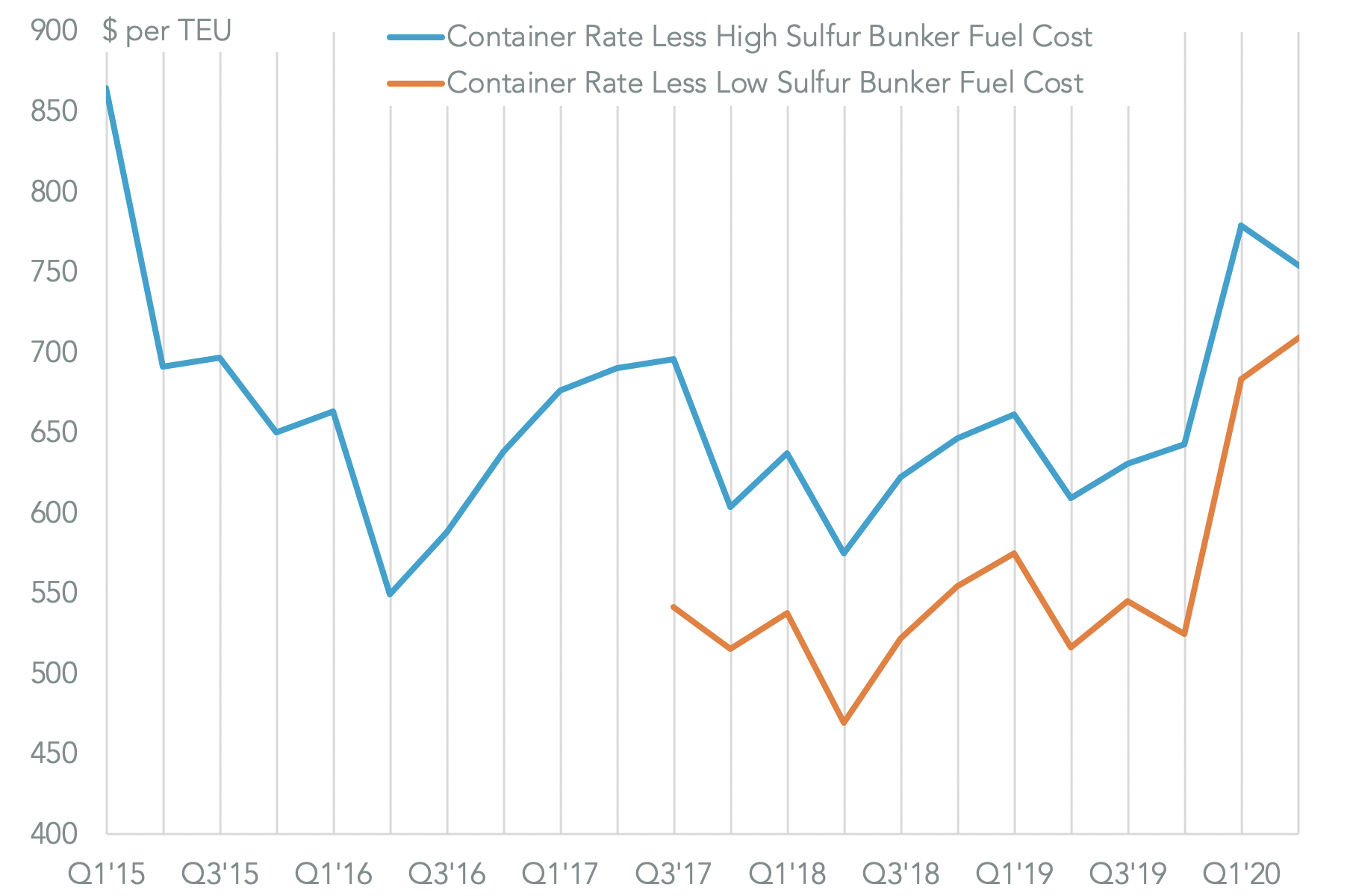

There’s certainly a precedent in terms of sulfur emission costs. From January 1 container lines had to either shift to low sulfur fuel or invest in scrubbing systems. While there is only a few months experience it appears that the increased costs have largely been passed through.

Average bunker excluded rates in Q2’20 using low sulfur fuels were around $710 / TEU, while rates using high sulfur fuels averaged $650 / TEU in the 2015 – 2019 period, Panjiva’s analysis of S&P Global Platts and Shanghai Shipping Exchange data shows.

Source: Panjiva

The supply chains of manufactured goods such as Mercedes Benz cars and Nike’s apparel can be transformed by automation such as additive manufacturing as well as government policy regarding reshoring. Clarity on the outlook for the latter in the U.S. will become more apparent ahead of the general elections in November, as discussed in Panjiva’s Q3 Outlook.

The situation for food and home / personal care supplies is more challenging given the importance of shipping ingredients as well as the geographic provenance of foodstuffs within their supply chains. That may provide fewer supply chain restructuring options for Danone, Starbucks and Unilever within the group.

Panjiva’s data shows that Maersk handled around 5,000 TEUs of U.S. seaborne import traffic for Danone and around 2,400 TEUs Unilever in the 12 months to June 30. That included a 49.0% surge in shipments for Danone and a 156% increase for Unilever in Q2 as both increased their supplies in response to shifting consumer demand resulting from COVID-19.

A side benefit for Maersk may come from increasing the service offering and total volumes handled on behalf of the two firms as they begin restructuring. Maersk was the leading shipping line for both firms on U.S. inbound lanes in the past two months but only represented 37.9% of Danone’s volumes and 25.0% of Unilever’s. Hapag-Lloyd was the second largest in both cases and may need to consider similar environment-led policies.

Source: Panjiva

Update: Abstract updated on 7/23 to show 2050 as target date for net zero carbon.