Es

EsPanjiva Research took part in a webinar on Sept. 9 with S&P Global Ratings which looked at the future for, and resilience of, Asian supply chains in the wake of COVID-19. A recording of the event, targeted at an Asia-Pacific audience, will be available here while this report summarizes the presentations and addresses the questions asked during the event.

Our colleague from S&P Global Ratings, Shaun Roache, noted that:

– the return to economic activity from COVID-19 is underway, but policy normalization is some way off – the so-called “90% economy”;

– the high proportion of jobs in retail hospitality means it could take until 2022 for employment to return to normal;

– as a result wage and therefore price inflation will remain low; the Chinese economic recovery may not be self-sustaining;

– the U.S. and China have already been decoupling in terms of relative exposure of trade and GDP to each other since 2018 already due to the trade war;

– and the U.S.-China rivalry is more about technological development, including China’s ability to grow via productivity improvements, than trade-in-goods.

From a supply chain perspective, Panjiva noted that firms are in the midst of a recovery phase with respect to COVID-19 that features continued operational disruptions. The fourth phase of recovery, outlined in Panjiva’s Q3 Outlook, will see companies outline longer-term resilience enhancing plans though many won’t detail those for investors until later in Q4.

In terms of trade policy, “tough on China” rhetoric in the U.S. will continue to dominate ahead of the U.S. elections and won’t change after the elections other than a more multilateral approach if former Vice President Biden wins. More positively a wave of trade deals not involving the U.S., mostly importantly including RCEP, will continue a decades-long process of trade liberalization.

On China US relations – aside from energy and agriculture, which industries would benefit most from increased Chinese purchases?

It’s important to note that 55% of China’s purchase commitments for goods are outside energy and agriculture. Those are imported by private companies and so less under control of government policy. Some of the areas that have seen the fastest growth have included semiconductors and pharmaceuticals which are the high tech areas which U.S. policy has sought to restrict.

The aerospace sector has been left out in the cold so far, in part due to the impact of COVID-19 on travel but as well due to Boeing’s troubles and the Chinese government’s support for Comac. A handful of big orders could help China cross its purchase commitment targets.

Panjiva’s data shows that China has historically been one of the largest single-country buyers of U.S. aerospace products with $16.3 billion of imports in 2017 – the baseline year for the trade deal. That’s dropped to $6.21 billion in the 12 months to July 31 as a result of COVID-19 as well as trade-war related restrictions. Relations with Europe, which represented 2.8x the value of exports from the U.S. to China in 2017, remain more important.

The services sector is also included in the infamous $200 billion purchase commitment figure and accounts for $68 billion of the total. Progress on the financial sector and investment policy liberalization by the Chinese government is encouraging here though the data has a very high level of latency.

Source: Panjiva

How will the US tech sanctions on China affect the supply chain in China? How big is the impact? Given the highly integrated nature of Asia’s regional supply chains, do you think a US-China decoupling will also force a US-Asia, or Asia-China decoupling? Will Asia’s tech supply chains be able to reorganise self-sustainably if the US keeps pushing forward with its decoupling with China in the electronics industry?

It’s too early to determine the final impact of the Trump administration’s actions regarding restrictions of technology exports. So far only a handful of companies have been covered, albeit important ones including Huawei, though it’s likely that more will be in time.

We’re already seeing strategic reactions with China reportedly planning support for its semiconductor industry as part of the 14th Five Year Plan and with TSMC planning a new fabrication facility in the U.S.

Should the decoupling process in supply chains proceed further then Asian electronics firms may need to split internally into a China facing business and a U.S. facing business. That’s a long way down the line however.

There are signs of reconfiguration of global supply chains. How easy or difficult is this materializing? Are we looking at trends where global and centralized supply chains are a thing of the past and localization takes prominence?

The reconfiguration of supply chains is incredibly difficult and expensive: factory sites have to be sourced, permissioned and built; workforces have to be trained; products need to be certified; and logistics as well as other infrastructure need to be put in place. It’s therefore a matter of years not months to complete a factory move.

Companies have been more focused on cutting all-in, long-term costs that just focusing on tariff-related issues though the process has accelerated during the trade war between the U.S. and China – tariffs have not been in place for over two years.

In terms of globalization there may be short-term reactions in some countries to encourage a shortening of supply chains, particularly in medical supplies. In the medium-term diversification as a strategy to dealing with uncertainties such as pandemics remains important. In the longer term though we may see drivers to a net shortening of supply chains from: improved technology including automation and additive manufacturing; expanding in-market, for-market strategies for larger economies; and government national security and jobs policies.

The rise of Malaysia and Vietnam as beneficiaries of the trade war has been well documented, where else may have room to grow?

Thailand has been a beneficiary from the trade war in a similar way to Malaysia and Vietnam. Its integrated electronics supply chains may help it avoid some of the assembly-only issues that Vietnam faces in terms of U.S. tariff risks. Mexico has also done well as a result of reduced USMCA uncertainty and could grow further as a result of membership of the CPTPP trade region.

India is doing better, though that’s been more a function of in-market, for-market manufacturing than part of a diversion strategy for most companies. The Modi administration’s reliance on restrictive trade policy raises questions about the sustainability of the growth though a trade deal with the U.S. could be on the cards after the elections.

Indonesia is often overlooked, both as a beneficiary of the trade war as well as due to regional economic and trade growth. Historically its exports have been dominated by commodities with energy and vegetable oils representing 34.4% of the total while manufactured goods accounted for just 15.4% in 2018.

There’s already several electrical and electronics firms operating in the country whose exports to the U.S. could expand in response to the trade war as well as other policies. One example can already be seen in the supply of mobile phone base stations to the U.S.

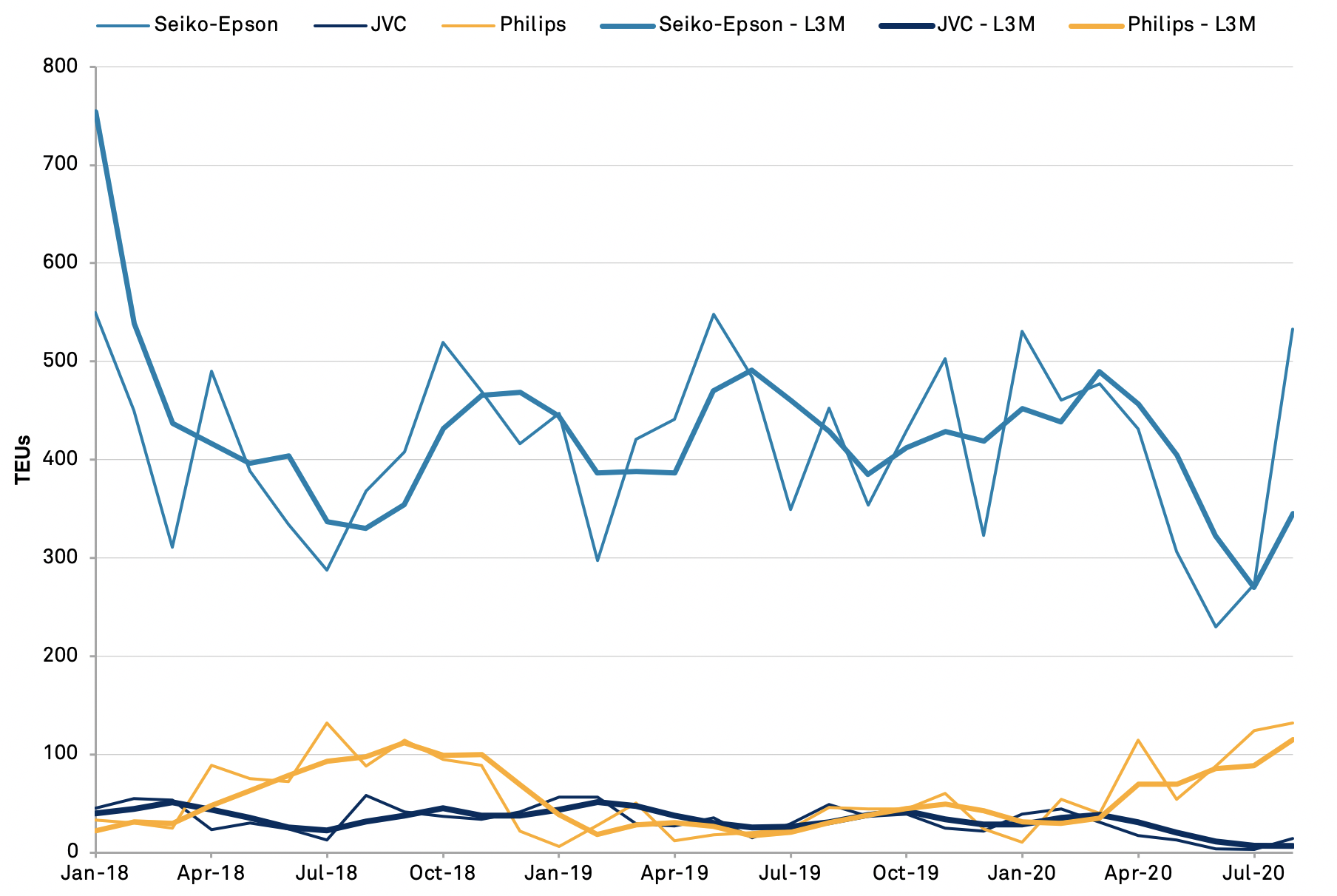

Panjiva’s U.S. seaborne import data shows that shipments of electricals and electronics (HS 84/85) from Indonesia have yet to take off. There was actually a 1.0% decline in 2019 versus 2018 while there’s been a 1.8% drop year-to-date in 2020 as of Aug. 31. There are already significant global players operating in the market though.

Exports linked to Seiko-Epson led the way with 4,800 TEUs shipped despite a 5.7% year over year decline. The situation has been more challenging for JVC in the wake of COVID-19 resulting in a 44.3% drop in shipments. There are new entrants and growth though with shipments of personal care products linked to Philips expanding by 202% year over year in 2020 so far.

Source: Panjiva