Es

EsAs the administration of President Donald Trump reaches the end of its first six months in office there has been considerable action on trade-related matters, but arguably the process of change has only just started.

President Trump has signed 42 items of legislation, though none of these related to trade, the New York Times reports. Instead he has relied on Executive Orders, memoranda and conventional trade reviews to start a series of processes that may impact 60.0% of U.S. trade (measured by total imports and exports) in the coming year, Panjiva data shows.

In large part these focus on reducing the trade deficit, which has is explicitly the main target for NAFTA renegotiations as outlined in Panjiva research of July 18. In that regards the data has been going the wrong way – the goods deficit increased 9.1% on a year earlier in May and is 10.0% above its pre-election level on a quarterly basis. It is, at least, down 2.8% vs. January.

Source: Panjiva

One major commitment that has been delivered on is to proceed with bilateral, rather than multilateral deals. The withdrawal from the Trans-Pacific Partnership back in January started the process, and has been replaced by a series of bilateral discussions with China, Japan, South Korea, India and Malaysia among others and the commitment to renegotiate of NAFTA. The latter will see talks start from August 16, and may last through the end of the year.

The challenge for NAFTA talks will be to find areas for the U.S. to expand exports outside the usual “E3A” (energy, agriculture, autos and aerospace) that dominate U.S. exports NAFTA and have been a focus for other trade talks. The four sectors accounted for 31.7% of U.S. exports to its NAFTA partners in the 12 months to May 31. Talks will also be complicated by non-goods issues including services, digital trade, labor and environmental standards and regulatory measures such as the dispute panel.

Source: Panjiva

The Trump administration has also successfully kicked off a new round of trade talks with China under the Comprehensive Economic Dialogue. The first 100 days yielded a 10 point plan including increased LNG and beef exports, as well as financials and services-related concessions. This process will need to be continued to ensure the Chinese trade surplus is turned around. Exports of LNG and beef could be worth $2.4 billion annually, equivalent to 0.1% of the Chinese trade surplus with the U.S.

Unfortunately, the round of talks on July 19 failed to make significant further progress. No new product initiatives emerged, though a commitment to continue talks in the coming year and a reaffirmation of a desire to cut the U.S. trade deficit were forthcoming. That comes as the Chinese trade surplus (Chinese definition of exports and imports) vs. the U.S. hit its highest since October 2014, and was 46% bigger than its surplus with the rest of the world combined.

Source: Panjiva

Talks to renegotiate limited elements of the KORUS trade deal with South Korea have been requested and may start in August. The simplest issue to address – yielding potential gains in U.S. exports without triggering a full renegotiation under U.S. TPA rules – would be the disparity in automotive shipments.

While there are barriers – particularly on inspection levels – to remove that does not guarantee Korean buyers will actually want to purchase U.S. vehicles. U.S. exports to the South Korea were 58,120 vehicles in the past 12 months to May 31, while South Korean exporters including Hyundai and Kia shipped 1.30 million to the U.S.

Source: Panjiva

The administration has put in place the groundwork for action with other countries. The Omnibus Report on the causes of the trade deficit, alongside the performance review of trade deals (due October 29) and the “ Made in America” impact of trade deals (due September 15) will provide the evidentiary backing for action. Meanwhile, dialogue processes with Japan, India and Malaysia should eventually result in firm policy actions – possibly along the lines seen with China.

The timings here are highly uncertain – the Omnibus report was scheduled to be presented to the President by June 29, but as yet nothing has been made available publicly. If anything it may open up new fronts in trade discussions, particularly with Vietnam which has been the third largest contributor to the expansion in the trade deficit over the past five years.

Source: Panjiva

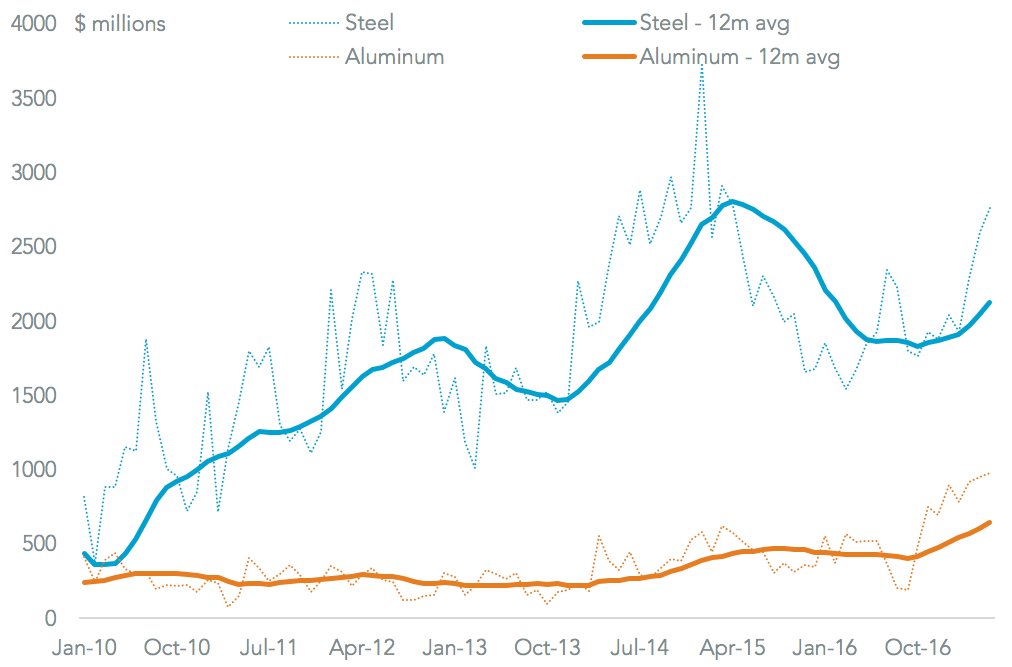

The largest outstanding to-do for the administration is to take action on imports of steel and aluminum under twin “section 232” reviews of the national security aspects of those industries. While the formal deadline for these reviews is January 15 and January 22 2018, action has been expected since the end of June. In the meantime the U.S. deficit in aluminum hit its highest since at least 2009 in May and steel’s the highest since March 2015.

Source: Panjiva

The Commerce Department has 39 product- or industry-specific trade cases ongoing, including two “section 201” safeguarding reviews. These are designed to protect an industry more broadly, and allow the President to take direct action on cases. ITC hearings on the cases are due on August 15 for solar power and September 7 for washing machines. Other sensitive cases, from a NAFTA perspective, are outstanding in aerospace and lumber with Canada, while a case involving sugar with Mexico has been resolved.

Taking the four largest cases together ( solar, washing machines, lumber and aerospace) there are $19.1 billion of annual imports that could be cut – though that is already 14.4% lower than a year earlier. Several cases, in steel and other sectors, have actually been delayed at the request of petitioners potentially looking for harsher outcomes.

Source: Panjiva